Theory of Dominant Money. Part I

Taxonomy of Money and Monetary Tide Changes

Dominant currency and dominant money

The approach of dominant money as outlined in this paper has in a way been inspired by theories about the internationally dominant currency as developed in recent years by Gopinath and colleagues, Eichengreen and, prior to them, Hudson.[1] Those theories deal with the dominant role of the US dollar in today's international currency system. Dominant money, by contrast, deals with the rise and decline of means of payment.

The use of the terms currency and money partly overlaps. In certain cases currency and cash can be used interchangeably. In this paper, 'currency' means an official monetary unit of account, while 'money' refers to the means of payment denominated in a particular currency. An occasional overlap in word usage cannot entirely be avoided.

In Gopinath et al., the dominant currency paradigm says that export-import-prices are most often set in the dominant currency and tend to be unvaried regardless of bilateral exchange rates.[2] In this respect, the dominant currency paradigm is about pricing in the dominant currency.[3] More generally speaking, the dominant currency is that in which most international prices are quoted and transactions invoiced (85% in US dollars, even though the US accounts for just 15% of international trade). Equally, most international finance contracts are concluded in the dominant currency. Presently, two thirds of the international debts of non-banks are denominated in US dollars (in euros one fifth).[4] Furthermore, the US Federal Reserve and the American banking sector control the dollar-based international payment systems.

The dominant currency also serves as the preferred reserve currency. Presently, the US dollar accounts for 64% of international currency reserves. The euro accounts for 20%, yen and pound 4% each. The Chinese yuan presently accounts for 1.2%, although it looks poised to become significantly more important in the decades to come.[5] Individual countries may peg their currency to the dominant one as this helps them avoid foreign exchange risk. They thus suspend monetary sovereignty, which from the perspective of a small or weak currency is relative anyway.

Dominant money cannot be defined by simple analogy. For example, the oft-quoted store-of-value function of money seems to be an analogy with the reserve function of lead currencies. In actual fact, however, the store-of-value function of money has shrunk today to holding enough liquidity for expenditure in the near term. Holding liquid money long-term would be hoarding money. This might still cause problems even under modern conditions of freely creatable fiat money, but in actual fact the medieval and early-modern problem of hoarding hardly exists anymore, certainly not under conditions of business-as-usual. Keynes' successor approach to hoarding – liquidity preference – is not about a general shortage of money, but about the fluctuating willingness of actors to spend, lend and invest. Store-of-value assets today normally take the form of capital invested in the short and long term.

The dominant money within a currency area is that which is system-defining during a certain historical period, in that it determines how the monetary system and monetary policy work, and which has the lead in creating money and readjusting its stock. Since money needs a quantity lever to exert dominance, the dominant money accounts for the biggest stock of money. Today this applies to bank deposit money – bankmoney for short. Liquid bankmoney is generally known as sight deposits, or demand or overnight deposits. Depending on the country, bankmoney represents 80–95% of the money in public circulation (M1).

Monetary dominance can also be seen empirically in the biggest share of payments in number and volume of transactions. From this angle, the picture is more varied, but basically still the same. For example, many everyday household transactions may still be carried out in small amounts of change, while wholesale transactions and generally almost all payments made by firms and public households have been cashless for long – thus carried out in bankmoney. In financial transactions, MMF shares have gained significantly in importance since the 1980/90s, while their role in payments for goods and services has remained marginal.

Taxonomy and hierarchy of money

A particular type of money constitutes a particular money circuit. The money in one circuit can basically be changed into another type of money; except for central-bank reserves and bankmoney that cannot be exchanged for one another. This is because the present system rests on the two-tier structure of banks and central banks. The banks provide bankmoney for non-banks (the money using public), while the central banks provide reserves (central-bank money-on-account) for the banks. The two-tier structure thus involves a split circuit, consisting of the public circuit of bankmoney among non-banks, tied to, but separate from, the interbank circuit of central-bank reserves. If customer A of bank X makes a cashless payment to customer B at bank Y, bank X transfers the amount in reserves to bank Y, while the same amount of bankmoney is deleted by bank X in the current account of A, and re-created by bank Y as a booking entry into the current account of B.[6]

Solid cash – comprising treasury coins and central-bank notes – traditionally represents a circuit of its own. At source, however, money today is non-cash bankmoney, or central bank reserves, respectively. Rather than cash still being the constitutive base for bankmoney, cash has long been an exchange quantity of bankmoney, in that cash is withdrawn from a bank transaction account and reconverted into bankmoney at some other point in time. However, as cash represents base money by its historical and institutional origin, banks still need to finance cash at 100%, whereas bankmoney creation only needs a small base of central-bank reserves.

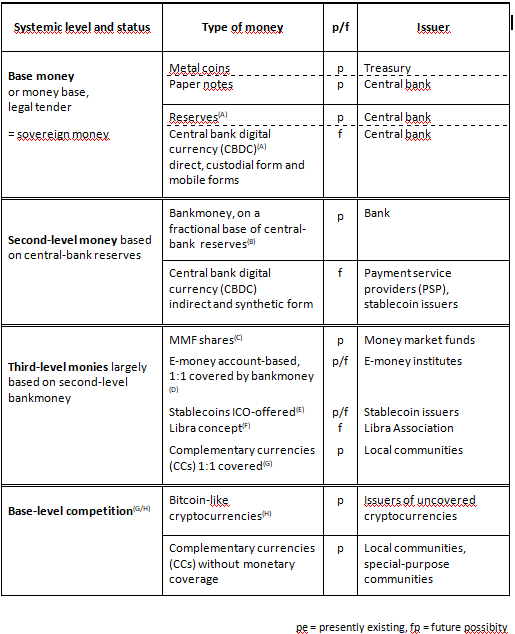

One ought to be aware of the different levels of moneyness as shown in the taxonomic overview of relevant types of money given in Table 1. Money issued by a treasury or central bank is base money. It makes up the money base. Second-level bankmoney is based thereupon. In recent decades, additional types of money have emerged, largely based on bankmoney, thus being third-level monies such as money market fund shares (MMFs), e-monies and cryptographic stablecoins, as well as complementary currencies (CCs). Uncovered private cryptocurrencies as well as central-bank issued digital currency (CBDC) represent additional new types of money.

Table 1 Taxonomy and hierarchy of money

The taxonomy rests on two defining dimensions. One is the technical form of the money, that is, coins, paper notes, digital deposit money (money-on-account), mobile money and cryptographic tokens. The other dimension is the money issuer, that is, treasuries (coins), central banks (notes and reserves), banks (bankmoney), and non-bank financial institutions (FI), other private agencies and local communities (third-level monies and base-level challengers).

The different types of money are issued in different ways. Solid coins are sold for central-bank balances and represent genuine seigniorage. Central-bank money and bankmoney are issued today in conjunction with the extension of loans, as well as in the form of bank and central-bank purchases of securities. According to current plans, CBDC is to be issued in 1:1 exchange for already existing central-bank money, while current third-level monies are bought in 1:1 exchange for second-level bankmoney.

The explanations for Table 1, related to letters A–H, are as follows.

(A) Central-bank reserves and future account-based CBDC are the same type of central-bank money, albeit relating to two different functions in the present system. The 'reserve' function serves as central-bank deposit money for interbank payments only. The other function, currently referred to as account-based CBDC, will provide the same type of central-bank money also to non-banks. Speaking of 'reserves' beyond reserve banking no longer makes sense.

(B) The liquid or active part of bankmoney (in M1) represents the overnight liabilities of the banks to their non-bank customers. The inactive, i.e. temporarily deactivated, part of bankmoney includes savings and time deposits (in M2, M3, depending on the currency area). To the extent that M2/M3 deposits can be liquidated at any time, they are not appropriately registered.

(C) MMFs are investment trusts that put the investors' bankmoney into short-term treasury bills and other highly rated securities. The shares can be used as a deposit-like means of payment, particularly in financial transactions.[8] This doubles the invested amount, in that the MMF shares can be used by the investors as a money surrogate, in addition to the paid-in bankmoney which is used by the trust. MMF shares are also known as shadow money.[9] However, respective authors consider not only MMF shares to be shadow money, but also overnight repos and asset-backed securities. These securitisation vehicles, however, are not used as money, but help provide liquidity by mobilising capital prior to final maturity, thus accelerating the circulation of money.

(D) E-money is a means of payment issued by a licensed e-money institute 1:1 against bankmoney (in most cases) and used in payments to third parties. Depending on

e-money regulation, the paid-in amount of money may have to be held in full, or may partly be invested in interest-bearing bonds. In the latter case, similar to MMFs, the money supply is extended, in that both the issued e-money and some part of the 1:1 bankmoney coverage are in circulation.

An example of e-money based on bank balances is M-Pesa (meaning 'mobile cash'), set up in 2007 in Kenya and in the meantime also in other countries. Thousands of M-Pesa agents, mostly small retailers, convert (and reconvert) cash paid in by customers into accounting units of the operating mobile phone company. The paid-in money is held by the involved telecoms in a commercial bank account (thus in bankmoney). The accounting units are airtime units worth the respective amount of money. Available airtime balances are transferable real-time and directly from payer to payee (P2P) via an app. The service is comparatively expensive.[10] Tigo Cash is a similar system offered in a number of Latin American and African countries, but transferring currency units rather than airtime.[11]

(E) Stablecoins ICO-offered. ICO stands for Initial Coin Offering, by analogy with the Initial Public Offering of stocks. It means that the units of a cryptocurrency are traded 1:1 for bankmoney, usually in US dollars. Accordingly, the exchange rate of a respective stablecoin is pegged to the dollar. Hence the claim to be a 'stable coin' in contrast to the high volatility of uncovered cryptocurrencies such as Bitcoin. 1:1 stablecoins represent e-money in the form of a crypto token.[12] Current stablecoins include Tether, USD Coin and JP Morgan Coin.

(F) The Facebook-initiated Libra is planned to be a stablecoin, too, 1:1 based on money and financial assets denominated in a basket of lead currencies. It was announced that 50% of the Libra currency basket would be denominated in US dollars, the rest split between euro, yen, pound and Singapore dollar. Even if based on national currencies, a supranational currency like the Libra would soon become systemically relevant and even superior to the basket currencies, exactly due to its being supranational and involving a clientele that potentially accounts up to one billion worldwide or even more. This might help maintain the US dollar's status as the dominant currency, but – similar to what happened with bankmoney – it might place the US Treasury and Federal Reserve in a subordinate role, with little choice but to re-act to the facts pro-actively created by the Libra.

(G) A complementary currency (CC) is most often issued not-for-profit in the form of simple paper scrip by some community or municipality as local money or special-purpose money, 1:1 against domestic bankmoney. CCs are unregulated, and thus free to proceed with the coverage as they wish.

(H) Bitcoin or Bitcoin-like cryptocurrencies have no money base or coverage. They claim to be money by their own fiat. In the case of Bitcoin, a 'coin mining' algorithm produces the crypto coin supply which is approximating a quantity limit similar to a gold standard at a fixed maximum of available gold. A number of successors to Bitcoin have scrapped that limitation.

The moneyness of private cryptocurrencies is unsettled. Stablecoins complying with e-money regulation can hardly be denied to be money (assuming they achieve a certain degree of circulation as a means of payment). This would also apply to the introduction of Libra.[13] Bitcoin, by contrast, although a number of international companies now accept it as a means of payment, continues to be treated as an instrument of speculative investment, not as money or a currency, respectively. Basically this applies to all crypto tokens not covered by a 1:1 reserve.

(G/H) If issued without monetary base or coverage, CCs and cryptocurrencies enter into immediate competition with the official national currencies. Central banks and governments have so far not seen this as a threat to monetary sovereignty, because there are many competing currencies accounting for relatively small amounts of money so far. In December 2019 the biggest 2,400 cryptocurrencies mustered a total market capitalisation of around USD 200 billion.[14] This may sound like a lot, but is only a small percentage of the cash and bankmoney that account for many trillions worldwide. The quantities of CCs are next to negligible.

Tidal changes in the composition of the money supply. Like ebb and flow[15]

The composition of the money supply has undergone changes throughout the ages. The rise and decline of a particular type of money can be likened to the rising and falling of tides. The last one of such tidal changes is shown in Figure 1, the rise of bankmoney, the major part of it in the course of the 20th century, from about a third of M1 to 90–95%. The rise came in two steps. The first was the era of 19th century imperialism and international free trade that ended with WWI and the Great Depression of the 1930s. The second step started with the recovery after WWII, entering a new era of economic growth and gradually liberalised international trade and finance. The final stage of it, globalisation, reached its peak in 2010–15.[16]

Figure 1 The rise of bankmoney to dominance

Figure 1 shows the respective pathway in Switzerland, but despite a certain degree of non-synchronicity among industrial nations, development took a comparable co-directional path in all old-industrial countries. Figure 2 shows the same graph, but vertically reversed, pointing out the decline of central-bank money, here in the form of solid cash.

Figure 2 The decline of central-bank money

The US seems to be an exception, in that cash represents about half M1 today, as much as bankmoney. Appearances can be deceptive. Cash accounted for only 20% of US M1 already in the 1950/60s.[17] The share then has risen continuously together with the rise of the US dollar as the dominant world currency. Most dollar notes are not used inside the US, but abroad as a parallel currency, as a cash safety cushion, and also as a worldwide underground currency. Since about 2010 the latter part has increasingly been taken on by Bitcoin and other cryptocurrencies. At the same time, the borders between M1 and M2 (savings and time deposits) have been blurred by quick availability of M2 balances so that these are preferred as far as possible. On top of this, bankmoney (demand deposits) has partly been replaced and generally outstripped by MMF shares up to 2.4 times M1.

Prior to the contemporary high tide of bankmoney and the low tide of central-bank cash and reserves, there were two other such tidal changes in the composition of the money supply in the Modern Age, and another is emerging right now:

From the 1660s until around the middle of the 19th century

/ rising tide of unregulated paper money

\ incipient decline in the systemic importance of sovereign coin

From around the middle of the 19th century until the 1910s

/ rising tide of central-bank legal tender notes

\ ebb tide for private banknotes

From the late 19th century until the early 2000s (as shown in Figures 1 and 2)

/ rising tide of bankmoney

\ falling tide for central-bank money

Upcoming from the 2020s

/ rising tide of sovereign digital currency (CBDC)

\ beginning ebb tide for bankmoney.

'Tide' is an illustrative abstraction. It simplifies, in that the path of real developments is never as straight or without deviation or backlash as the abstract idea suggests. Similarly, the tidal changes in the money supply do not mean there was always an absolute decline in the quantity of a particular type of money as was the case with medieval tally sticks and early-modern unregulated banknotes. In contrast to these, the stocks of coins, paper money and reserves kept growing until the recent past, corresponding to continued growth of the population and the economy. However, the share of a particular type of money in the composition of the money supply (e.g. central-bank notes, bankmoney), as a percentage of the total, was increasing during a particular historical timeframe from a low level upwards, and decreasing in a later era from the highest level achieved (e.g. coins, central-bank notes and central-bank reserves).

In Galbraith there is a discussion of tight versus loose money, with the pendulum of opinion and policies swinging back and forth between the two.[18] In a similar way, Skidelsky compares hard and soft money theories and discusses various historical shifts from one to the other.[19] Such changes certainly refer to a fundamental question of monetary policy in modern times. The question of scarcity and over-abundance of the money supply also plays a role in the monetary tide changes discussed in this paper. The latter, however, are not about fluctuating attitudes in economics and monetary policy in the first place, but about the rise of new types of money and their subsequent relative decrease or even fall.

The discussion of monetary tide changes that follows allows assuming that a significant shift in the composition of the money supply occurs

(1) if the incumbent dominant money poses problems that cannot be solved within the monetary framework of the time and/or

(2) if a new type of money emerges that offers at least a partial solution to the problems, or comes with other advantages, particularly lower costs of provision and handling in combination with improved ease of use and transferability (speed of circulation and overall efficiency of settlements). So far, one can say that incumbent monies were less convenient, circulated at lower use frequency, and were more expensive to provide and handle than the competing new monies.

From the 1660s to around the middle of the 19th century: rising tide of unregulated banknotes, incipient decline in the systemic importance of sovereign coin

Pre-modern currencies were coin currencies (leaving aside the medieval history of tally sticks). The typical shortcoming of coin currencies was chronic paucity of silver and gold. The coin shortage was not really reduced by the influx of silver and gold from Latin America, known as the Spanish silver inflation. It started in the 1560s and lasted for over hundred years. Prices rose in Spain and other affected regions – even if moderately, compared with the inflation surges of the 20th century – because real economic supplies could not keep pace with the money supply.

The overall coin shortage was exacerbated by the practice of hoarding precious metal coins, often secretly to hide the money from the tax collector. Furthermore, the shortage and hoarding of coins induced recurrent phases of coin debasement. One practice was 'decrying' the coins time and again to re-mint and re-issue them at the same face value but with lower silver content. This also happened in an undeclared and fraudulent manner. The last era of intensified debased coinage was during the Thirty Years' War (1618–48). Coin debasement in turn came with uncertain acceptance of various coins, resulting in unstable value parities.

This then was the background for the first rise of a new type of modern money which occurred since the 1660s to around the middle of the 19th century. That time saw the rising tide of paper money. Silver and gold remained predominant overall, but experienced a relative loss of monetary significance over time. Paper money offered an answer to the natural scarcity of silver and gold, to the hoarding of coins, and the recurrent debasement of coinage. Paper money can easily be written out or printed in any quantity. Paper money need not be scarce.

Banknotes may partly be covered by silver and bullion, but they do not have 'intrinsic' commodity value. And yet, to the degree they are accepted in lieu of coin, they give full purchasing power. Paper money opened the door to monetary modernity by substituting a purely symbolic or informational token for the traditional commodity money. This does not contradict Keynes' view of stamped silver coins to have always been token money. With paper money, however, modern money was starting to break away from its traditional commodity substrate.

Paper money was much cheaper to produce and more convenient to handle than the cost-intensive mining, melting, minting and handling of coins and bullion. The related seigniorage for note issuers was accordingly much higher. Payment of larger amounts of money in banknotes carried in a wallet was more convenient than payment in coins carried in belt bags and strongboxes.

However, paper money made it possible to counterfeit the notes, succeeding the previous fraudulent coin debasement. Forgery of paper money even became a way of warfare by other means, in this case as an assault on the enemy's currency. For example, English counterfeiting helped wreck the continental dollar notes of the American War of Independence as well as the assignats of the French Revolution. The Nazis tried to do likewise in 1943/44 when they forced highly skilled concentration camp prisoners to counterfeit British pound notes. The effect, however, was not that important anymore as most large transactions had long since been cashless.

The banknote issue was licensed by the respective treasury or parliament. The note-issuing banks were private companies, even if privileged by the Crown or a local principality. Typical cases included the Stockholms Banco 1656/61, the Bank of England 1694, and the Paris-based Banque Générale 1715 run by John Law. The Amsterdamsche Wisselbank 1609 and the Hamburger Bank 1619, modelled after early-modern Italian banks, initially did not issue banknotes, but served giro banking for merchants.

In the course of the 18th century German principalities began issuing uncovered treasury bills – pure fiat money. They came under different names, for example, Cassen-Billets of the Kingdom of Saxony, and were used like banknotes. They were issued by way of government expenses for public works, the military and civil servants, and they could be used for payment of taxes which helped make them more widely accepted domestically.

In America at the same time, and also due to a lack of coins, the governors of what were to become the later Federal States issued uncovered colonial bills, also known as colonial scrip, to every taxpayer free of interest and redemption. In most cases, the practice did not cause inflation, in a few cases only to a small extent. Instead, the bills triggered a surge in prosperity. The practice was restricted by British Currency Acts between 1751 and 1773. The Americans' rancour over this economically damaging restraint can be seen as a main reason behind the ensuing War of Independence.

The paper money of the time came as a mix of state-issued notes, state-privileged private banknotes, and purely private banknotes, the mix depending on the country and time. What they had in common was that they were largely unregulated. Even treasury-issued notes were not 'legal tender', a notion which only came into existence in the course of the 19th century. Except for the licensing of the note issue there was no coherent idea of a monetary regime for banknotes, although everyone knew that over-issue had to be avoided. It appears the American governors at the time were by and large successful in striking a balance between too little and too much. This could not be said of the note issue of the Banque générale under John Law and his card-table companion, the Duc d'Orléans, nor of the assignats of the French Revolution.

Paper money had certainly allowed for a much increased money supply in support of the growing goods manufacture and trade of the mercantile era. However, the multitude of paper notes, issued by individual banks and principalities, often of only local reach and uneven trustworthiness, meant the varied and overall limited acceptance of the banknotes. A similar problem was the convertibility of notes into silver coin, which was promised but not always kept. The lack of universal acceptance was the Achilles' heel of unregulated paper money from the beginning. Throughout the 18th and far into the 19th century the patchy acceptance of paper money hampered the development of well-integrated national markets and also international trade.

Furthermore, and also from the beginning, the ease of issuing notes lured bankers and certain treasuries into over-issue of paper money based on fractional reserves of coin and bullion. This in turn resulted in unstable currency exchange rates and unstable purchasing power, as well as banking crises and hitherto unknown boom-and-bust-cycles.

From around the middle of the 19th century until the 1910s: rising tide of national central-bank notes, full ebb tide for unregulated banknotes

The second monetary tide change was from 1833 (England) and the following decades until the 1910s (WWI). This era was the rising tide of national central-bank notes and the full ebb tide for unregulated paper money, particularly private banknotes. They were phased out, while central-bank notes were phased in, establishing the legal-tender note monopoly such as it stands to the present day. The transition from unregulated paper money to legal-tender notes was a gradual process lasting decades, but in the end there were no more private banknotes, and central-state treasury notes only to a small extent. Central-bank notes became the dominant type of money in this period. The central-bank note monopoly resolved the problems of unregulated notes of diverse origins. Central-bank notes proved to be a useful universal means of payment, accepted everywhere by everyone in payment of whatsoever. National banknotes were the means of choice to build nationally integrated economies.

However, there was a catch: the gold standard. It was made the fundament of the new note regime at the insistence of the British bullionists from around 1810 who had accused the Bank of England of over-issue of notes. The gold standard intended to limit the creation of central-bank notes according to existing gold stocks, in this way artificially reproducing the natural scarcity of precious metal coins. At the time, this was thought to be an anchor of stability, and was seen that way for a long time, even as late as 1944 in Bretton Woods when the gold dollar was established, rather than recognising any gold standard with Keynes as the 'barbarian relic' it is.

In actual fact, the gold standard proved to be a backward-looking hindrance to providing for the expansive needs of the time (population growth, urbanisation, industrialisation, national and international trade). The gold standard was a basically deflationary setback contributing to unnecessary bottlenecks in the allocation of funds and distribution of income, adding to pauperism and social class antagonism.

The British Currency School of the 1830–40s had played a decisive role in establishing the central-bank note monopoly. They were opposing the private-money Banking School of the time. The legal basis for central-bank notes was created with the Bank of England Act in 1833 and the Bank Charter Act in 1844. This then, including the gold standard, became the point of reference for most European states at an 1867 meeting in Paris. Central-bank notes are still about paper money, but monetarily they represent a different type of money: legal tender, sovereign money, issued by the national central bank on the basis of a legal mandate.

Things developed differently in the United States. After two discontinued attempts to establish a licensed private central bank, the US Treasury under Lincoln's presidency started to issue uncovered legal-tender notes in 1862 to pay for the expenses of the Civil War, the still famous 'greenbacks', mirrored on the Confederate side in the issue of 'greybacks'. The issue of US Treasury notes has only been discontinued between the mid-1960 to the mid-1990s, but they are still valid legal tender side by side with Federal Reserve notes since 1914. The Federal Reserve was set up on the initiative of a group that was known at the time as New York international bankers, and it still is a corporate enterprise. Over time, however, its most important functions – top personnel, monetary policy, and seigniorage – were regulated by public law and are carried out with Treasury participation. So, the final outcome of the developments in America and Europe was co-directional despite not unimportant institutional and legal differences.

From around 1900 until today: rising tide of bankmoney, ebb tide for central-bank money

The third monetary tide change took place from the decades around 1900 until today. We live at the end of this era, determined by the rising tide of bankmoney and the ebb tide for central-bank money as shown in Figures 1 and 2.

The reason for this tidal change was not a problem with the note monopoly. The problem was the gold standard. It caused artificial scarcity of money amidst strongly growing populations, industries and trade. As a result, the gold standard repeatedly had to be relaxed or even temporarily suspended. An amount of national treasury bonds were counted as part of the 'gold' coverage of the stock of central-bank notes.

More importantly, as an alternative to cash and a way to bypass the restrictions of the gold standard, the practice of interbank clearing of claims and liabilities was expanded. The practice dates back to long-distance trade by land and sea from the High Middle Ages to the Early Modern Age. The now more broad-based expansion of that practice strengthened the role of bank giro accounts, left unregulated in the paper money reforms of the 19th century, and established cashless interbank clearing as a general way of making payments, thereby turning bank deposit balances into non-cash money: the bankmoney such as it stands today. It took off in the decades before and after 1900, spreading more widely as 'chequebook economy'. The bank credit theory of money dates from the 1890s. The US and the UK were ahead of others in this development, but all industrial countries caught up soon.

Cashless payment practices were supported by ongoing innovations in telecommunication and data processing throughout the 19th and 20th centuries (postal services, telegraph, telephone, calculating and tabulating machines, telex, computerisation and the internet). Cashless payment is more convenient and cheaper than payment in cash, particularly in wholesale banking when many or large payments are involved. Balances of deposit money are easier and cheaper to provide and handle than banknotes. The money users had advantages in terms of convenience. Bankmoney is also safer to store and handle than notes and coins. Account balances cannot be falsified in the same way as paper notes can be counterfeited. In terms of technical and monetary efficiency, a cash-based money system cannot compete with technology-based cashless payment practices. So the path was established for the rise of bankmoney and its definite predominance after WWII.

The rise of bankmoney and the decline in central-bank money are two sides of the same process. The decline in central-bank money is even more pronounced than the pathway in Figure 2 would suggest. The greater part of the cash, as explained above, is not active domestically, but abroad and in the underground (particularly US dollars, to a smaller extent also euros) ll as abroad.[20]

Furthermore, which cannot be seen in the chart, there is the parallel decline in the banks' vault cash and liquid central-bank reserves necessitated by the banks to expand bankmoney and maintain its circulation. Coin reserves had always been only a fraction of private banknotes, and also central-bank reserves have always been only a fraction of today's bank deposit money. The fractionality of reserves has now reached an extremely low level. Banks in the euro area need to have available base-level central-bank money of just 2.5–3% of the stock of bankmoney, consisting of 1.4% vault cash, a 1% largely idle minimum reserve requirement, and 0.1–0.6% excess reserves, that is, active interbank payment reserves, depending on a bank's size.[21] In the US a hundred years ago, the amount of fractional excess reserves was 10–15% of the stock of bankmoney.[22] Today, that fractional percentage is down to between 0.1% (large banks) and 2–3% (smaller banks).

Minimum reserves no longer exist in the countries of the British Commonwealth and some other countries. In the US there is still a formal reserve requirement of 10% minus vault cash. However, many banks are unbound by reserve requirements. Certain positions such as large time deposits are generally exempt from the requirement. Banks are allowed to temporarily 'sweep' deposits to accounts that are not subject to reserve requirements. As a result, the actual US reserve requirements have 'rapidly been losing relevance' and are now near the reserve of vault cash.[23]

Considering that any bankmoney transfer is fully carried out in reserves in today's RTGS payment systems, how can the base of necessitated reserves be so small? This is possible due to a number of factors. The first of the three most important is that outgoing reserves from a bank are incoming reserves in other banks, so that the flows of reserves between the banks continuously offset each other, the more so, the fewer and larger the banks. Secondly, customer payments are spread over time and actors, transferring at any point in time only some part of the total stock of bankmoney. A third condition is the non-separability of client money from a bank's own money. All transactions are managed via one and the same central-bank account of a bank. The proprietary means of a bank (cash and reserves) cannot be attributed to a customer's money claims on that bank, and the bank's money liabilities to its customers are largely uncovered. Put pointedly: the clients' bankmoney is held hostage to the banks' balance sheets.

In seeming contradiction to the decline in required and necessitated reserves, an exceptionally high level of reserves has been built up since 2007/08, along with a persistently low level of interest. This flood of reserves is an anomaly rather than the new normal, the result of the central banks' crisis policies of Quantitative Easing (QE). The purpose of QE is stabilising bonds and financial markets. Providing liquidity to the banks was another reason, but only at the beginning when the interbank money market temporarily stopped functioning. Thereafter, the vast amount of reserves was reinterpreted to be an economic stimulus. This is misleading, because reserves cannot leave the interbank circuit. QE thus remained QE for finance only. If the banks really wanted to extend more credit according to real-economic demand, they can do so without needing a vast amount of reserves.

In a predictably futile attempt to stimulate expenditure nevertheless, some European central banks, including the ECB, have resorted to the counter-productive policy of imposing negative interest on the reserves held by the banks. (The Federal Reserve and the Bank of England did not do so with good reason). The reserves have thus become 'hot potatoes' the banks would like to pass on but cannot easily get rid of. So far, the ECB has not reabsorbed reserves by reselling bonds. For the banks, the alternative of putting more of the reserves into foreign investment poses an additional exchange rate exposure. Apparently, QE for finance as well as the unprecedented low or even negative interest rates are an expression of the dead end of monetary policy at the height of the problem- and crisis-ridden bankmoney regime.

The rise of bankmoney – which emerged and took off also in circumvention of the gold standard – was accordingly accompanied by the stepwise abandoning of the gold standard from WWI to WWII. The subsequent gold-dollar standard agreed upon in Bretton Woods 1944 was soon softened again and finally terminated in 1971, to give way to what has developed into the 'US treasury bill standard'.[24] This then lifted the boundaries of monetary quantities and enabled hitherto unknown economic growth and comparatively broad-based wealth in industrialised countries. The downside was – similar to unregulated paper money in the 18th century, but on a larger scale – that bankmoney also unleashed new excess dynamics of overshooting money creation and the related continued growth of credit and debt in increasing disproportion even to nominal economic output, resulting in increased inflation and/or asset inflation, financial instability and proneness to crisis.

Banks have the pro-active lead in money creation. The central banks re-act and re-finance fractionally, in fact always, even if at different lending interest which, however, is not decisive as the interest is relevant only to a small fraction of the bankmoney. This being the case, the banking sector largely determines the entire money supply, when it's too much, and also when it's too little. The remaining quantities of cash and reserves have over time become a subset of the quantities of proactively created bankmoney. The fractionality of operationally necessitated reserves together with the proactive lead of the banks in money creation explains why bankmoney was able to become so dominant despite its being second-level money and its dependence on being refinanced (fractionally) by base-level central-bank money.

With cash now getting out of use sooner or later, and operationally necessitated reserves down to a small fraction of bankmoney, the quantity lever of central-bank base rate policy has become worryingly short. At the same time, due to the general oversupply of money and capital, including obstructively high levels of indebtedness, interest rates are unnaturally low so that base rate policy has currently no meaningful effect on the economy.[25] The effectiveness of conventional instruments of monetary policy has been weakened, resulting in a far-reaching loss of monetary control. QE for finance only – an exercise in quantity policy, by the way – has been effective, but primarily in postponing rather than solving the problems, adding to the non-GDP contributing parts of finance (particularly trade in real estate/housing, commodities, stocks and derivatives) as well as increased inequality.

Central-bank base rate policy cannot 'transmit' if central-bank money is operationally marginalised both in interbank and public circulation. Central-bank rates do not mechanically or even magically transmit themselves onto the rates of banks and capital markets. Central-bank interest rate policy needs a quantity lever. A central bank without important amounts of central-bank money in active interbank and public circulation might look redundant, a little like King Lackland.

Indifferent to both the far-reaching loss of monetary control and the crisis-proneness of the bankmoney regime, many experts and practitioners cling to believing in the self-regulation of markets. It helps a lot to reduce real-world complexity. In monetary and financial matters, however, there is a recurrent mechanism of market failure. The belief in efficient markets has a point, but is not the entire truth about markets. The belief can even be misleading, for example regarding prestigious club goods, conspicuous consumption items, and particularly financial markets. Markets are supposed to approximate a point of equilibrium thanks to a negative feedback loop in which higher prices lower the willingness to buy. If, however, buyers assume that a rise in prices will continue, then rising bid prices will prompt an equally rising preparedness to pay on the side of the buyers, propelling a positive feedback loop with open-end excess dynamics.

There is no doubt that the delimiting negative-feedback mechanism is at work also on financial markets. But it is repeatedly superseded by positive-feedback boom dynamics with ensuing financial market failure. Such positive-feedback dynamics is central to both the 'irrational exuberance' analysis in Shiller, as well as the financial instability hypothesis of Minsky[26] – and this is why financial markets under conditions of basically unrestrained creation of money, credit and debt cannot be expected to be self-limiting, and why there must be a monetary authority exerting control over the creation of fiat money and the spreading of money surrogates.

Upcoming from the 2020s: rising tide of sovereign digital currency (CBDC), incipient ebb tide for bankmoney

Bankmoney has accomplished its rise to monetary dominance, but again, as in the tidal changes before, the dominant bankmoney regime is unable to solve the problems it creates, including the inability of central-bank monetary policy to do much about it as long as the underlying composition of the money supply and its excess dynamics remain unchanged. Considering the above problems, the bankmoney regime is approaching a state of ungovernability – a situation that cannot last. Another monetary tide change is dawning, likely to emerge from the 2020s and giving rise to sovereign digital currency (CBDC), as discussed hereafter in part II of this paper.

Footnotes

[1] Gopinath, Boz, Casas et al. 2016, Gopinath/Stein 2018, Eichengreen 2011 39–68, Hudson 2003 [1972], 2012 367–383.

[2] Gopinath et al. 2016, Gopinath/Stein 2018. On dominant currency pricing also cf. Carney 2019.

[3] Carney 2019.

[4] According to data by the Basel Bank for International Settlements. In 2008 the share of US dollar-denominated international debt was 50% (Eichengreen 2011 2, 68, 123).

[5] IMF Data, Currency Composition of Official Foreign Exchange Reserves, http://data.imf.org.

[6] For further explanations of how the present money system works cf. Ryan-Collins et al. 2012 28–88, Huber 2017 97–97, McLeay/Radia/Thomas 2014, Deutsche Bundesbank 2017.

[7] For a similar and more detailed taxonomy of 100% e-money and stablecoins see Hess 2019. For a taxonomy of cryptocurrencies cf. Bech/Garratt 2017 57–62 and Adrian/Mancini-Griffoli 2019 2–5.

[8] Baba/McCauley/Ramaswamy 2009, Hilton 2004, Mai 2015.

[9] Cf. Murrau 2017, McMillan 2014 65–80.

[10] Groppa/Curi 2019 5–6, 16.

[11] money.tigo.com.py, ayuda.tigo.com.py/hc/es/categories/201585128-Billetera-Electrónica.

[12] Cf. Hess 2019.

[13] https://de.slideshare.net/HermannDjoumessi/libra-whitepaper-english.

[14] https://coinmarketcap.com/all/views/all.

[15] The sources on the history of money behind this chapter include Aliber/Kindleberger 2015 [1978], Davies 2013 [1994], Ferguson 2008, Galbraith 1995 [1975], Graeber 2012, Hixson 1993, Huerta de Soto 2009, Kindleberger/Laffargue (Eds) 1982, North 1994, O’Brien 1994, 2007, Siekmann 2016, Simmel 1989 [1900], Skidelsky 2018, Zarlenga 2002.

[16] According to the KOF Globalisation Index by ETH Zurich.

[17] Currency component of M1, fred.stlouisfed.org/graph/?g=34Kf.

[18] Galbraith 1995 [1975] chapters 7, 8, 19.

[19] Skidelsky 2018 39.

[20] Esselink/Hernández 2017, Krüger/Seitz 2014.

[21] Macfarlane/Ryan-Collins/Bjerg/Nielsen/McCann 2017, Huber 2017 72–74.

[22] Fisher 2007 [1935] 52.

[23] Bennett/Perestiani 2002 53, 65.

[24] Hudson 2003 [1972] pp.377.

[25] Summers/Stansbury 2019, Turner 2019, Bordio/Hofmann 2017.

[26] Shiller 2015 pp. 175, pp. 226. Minsky 1982, 1986 pp. 206.

References

Aliber, Robert Z. / Kindleberger, Charles P. 2015 [1978]. Manias, Panics, and Crashes. A History of Financial Crises, New York: Basic Books. 7th edition.

Adrian, Tobias / Mancini-Griffoli, Tommaso. 2019. The Rise of Digital Money, IMF Fintech Note 19/01.

Adrian, Tobias / Mancini-Griffoli, Tommaso. 2019b. Digital Currencies: The Rise of Stablecoins, IMF Blog, Sep 19, 2019.

Adrian, Tobias / Mancini-Griffoli, Tommaso. 2019c. From Stablecoins to Central Bank Digital Currencies, IMF Blog, Sep 26, 2019.

AMI (American Monetary Institute). 2010. Presenting the American Monetary Act, Valatie, NY: American Monetary Institute, http://monetary.org/wp-content/uploads/2011/09/32-page-brochure.pdf.

Baba, Naohiko / McCauley, Robert N. / Ramaswamy, Srichander. 2009. US dollar money market funds and non-US banks, BIS Quarterly Review, March 2009, 65-81.

Barrdear, John / Kumhof, Michael. 2016. The macroeconomics of central bank issued digital currencies, Bank of England, Staff Research Paper No. 605, July 2016.

Bech, Morten / Garratt, Rodney. 2017. Central bank cryptocurrencies, Basel Bank for International Settlements, BIS Quarterly Review, September 2017, 55–70.

Bennett, Paul / Peristiani, Stavros. 2002. Are U.S. Reserve Requirements still Binding? Federal Reserve Bank of New York, Economic Policy Review, Vol.8, No.1, May 2002, 53–68.

Bindseil, Ulrich. 2019. Central bank digital currency - financial system implications and control, Working Paper, ECB Directorate General Operations, 30 July 2019. https:// ssrn.com/abstract=3385283.

BIS. 2018. Central bank digital currencies, prep. by the BIS Committee on Payments and Market Infrastructures, Basel: Bank for International Settlements, March 2018.

BIS. 2019. Proceeding with caution. A survey on central bank DC, Bank for International Settlements Papers, no. 101, Jan 2019.

Bjerg, Ole. 2017. Designing New Money – The Policy Trilemma of Central Bank Digital Currency, Copenhagen Business School Working Paper, June 2017.

Bjerg, Ole. 2018. Breaking the Gilt Standard. The problem of parity in Kumhof and Noone's design principles for Central Bank Digital Currencies, Copenhagen Business School Working Paper, August 2018.

Bordo, Michael D. / Levin, Andrew T. 2017. Central bank digital currency and the future of monetary policy, NBER Working Paper Series, no. 23711, Aug 2017.

Borio, Claudio / Hofmann, Boris. 2017. Is monetary policy less effective when interest rates are persistently low? BIS Working Paper, No. 628, April 2017, Basel: Bank for International Settlements.

Carney, Mark. 2019. The Growing Challenges for Monetary Policy in the current International Monetary and Financial System, Speech at the Jackson Hole Symposium 2019, publ. by the Bank of England, August 2019.

Danezis, George / Meiklejohn, Sarah. 2016. Centrally Banked Cryptocurrencies, http:// www0.cs.ucl.ac. uk/staff/G.Danezis/papers/ndss16currencies.pdf.

Davies, Glyn. 2013 [1994]. A History of Money, Cardiff: University of Wales Press.

Dawney, Emma. 2017. Sovereign Money Initiative. The background to the national referendum on sovereign money in Switzerland, on behalf of MoMo (Verein Monetäre Modernisierung), Zürich/Wettingen.

Deutsche Bundesbank. 2017. The role of banks, non-banks and the central bank in the money creation process, Bundesbank Monthly Report, Vol. 69, No. 4, April 2017, 13–30.

Dyson, Ben / Graham, Tony / Ryan-Collins, Josh / Werner, Richard A. 2011: Towards a Twenty-First Century Banking and Monetary System. Submission to the Independent Commission on Banking, available at: http://www.neweconomics.org/publications/ entry/towards-a-21st-century-banking-and-monetary-system

Eichengreen, Barry. 2011. Exorbitant Privilege. The Rise and Fall of the Dollar and the Future of the International Monetary System, New York: Oxford University Press.

Esselink, Henk / Hernández, Lola. 2017. The use of cash by households in the euro area, European Central Bank Occasional Paper Series, No. 201, Nov 2017, Frankfurt.

Ferguson, Niall. 2008. The Ascent of Money. A Financial History of the World, London/New York: Allen Lane.

Fisher, Irving. 2007 [1935]. 100%-money, New Haven: Yale University; reprinted in William J. Barber et al. (eds.) 1996: The Works of Irving Fisher, London: Pickering & Chatto.

Galbraith, John Kenneth. 1995 [1975]. Money. Whence it Came, Where it Went, New York: Houghton Mifflin. 1st ed. 1975.

Goodhart, Charles A. E. 1998. The two concepts of money – implications for the analysis of optimal currency areas, European Journal of Political Economy, 14 (1998) 407–432.

Goodhart, Charles A.E. / Jensen, Meinhard. 2015. Currency School versus Banking School: an ongoing confrontation, Economic Thought, 4 (2) 20–31.

Gopinath, Gita / Boz, Emine / Casas, Camila / Díez, Federico J. / Gourinchas, Pierre-Olivier / Plagborg-Möller, Mikkel. 2016. Dominant Currency Paradigm, NBER Working Paper, No. 22943, Dec 2016.

Gopinath, Gita / Stein, Jeremy C. 2018. Banking, Trade, and the Making of a Dominant Currency, NBER Working Paper, No. 24485, April 2018.

Graeber, David. 2012. Debt. The First 5,000 Years, New York: Melville House Publishing.

Groppa, Octavio / Curi, Fernando. 2019. Mobile Money Regulation: Kenya, Ecuador and Brazil Compared, Working Paper, Buenos Aires: Universidad Católica Argentina.

Groß, Jonas / Herz, Bernhard / Schiller, Jonathan. 2019. Libra — Konzept und wirtschaftspolitische Implikationen, Wirtschaftsdienst, Sep 2019, Vol.99, Heft 9, 625–631.

GSMA. 2018. State of the Industry Report on Mobile Money, https://www.gsma.com/mobile-fordevelopment/wp-content/uploads/2019/02/2018-State-of-the-Industry-Report-on-Mobile-Money.pdf

Heasman, Will. 2019. The worrying truth behind China's digital currency, Decrypt, Dec 6, 2019.

Hess, Simon. 2019. 100% E-Money and its Implications for Central Bank Digital Currency, SSRN electronic journal, June 26, 2019.

Hilton, Adrian. 2004. Sterling money market funds, Bank of England Quarterly Bulletin, Summer 2004, 176-182.

Hixson, William F. 1993. Triumph of the Bankers. Money and Banking in the Eighteenth and Nineteenth Centuries, Westport, Conn./London: Praeger.

Huber, Joseph / Robertson, James 2000: Creating New Money, London: New Economics Foundation.

Huber, Joseph. 2017. Sovereign Money. Beyond Reserve Banking, London: Palgrave Macmillan.

Huber, Joseph. 2017b. The case for a central-bank currency register. Accounting for sovereign money on banks' and central banks' balance sheets, Working Paper, Nov 2017, available at sovereignmoney. site/how-to-account-for-sovereign-money.

Huber, Joseph. 2019. Digital currency. Design principles to support a shift from bankmoney to central bank digital currency, real-world economics review, issue no. 88, July 2019, 76–90.

Huber, Joseph. 2019b. Negative interest – hoping in vain for a miracle tool, working paper available at sovereignmoney.site/negative-interest.

Hudson, Michael. 2003 [1972]. Super Imperialism. The Origin and Fundamentals of U.S. World Dominance, new edition, London: Pluto Press.

Hudson, Michael. 2012. The Bubble and Beyond, Dresden: Islet Verlag.

Huerta de Soto, Jesús. 2009. Money, Bank Credit, and Economic Cycles, Auburn, Al.: Ludwig von Mises Institute, 2nd edition (1st 2006).

IMF. 2018. Casting Light on Central Bank Digital Currency, IMF Staff Discussion Note, Washington: International Monetary Fund.

Ingves, Stefan. 2018. The e-krona and the payments of the future, Speech by the Governor of the Swedish Riksbank, Stockholm.

Jackson, Andrew / Dyson, Ben 2013: Modernising Money. Why our monetary system is broken and how it can be fixed, London: Positive Money.

Juškaitė, Aistė / Šiaudinis, Sigitas / Reichenbachas, Tomas. 2019. CBDC – in a whirlpool of discussion, Lietuvos Bankas, Occasional Paper Series, No. 29, Dec 2019.

Kahn, Charles M. / Rivadeneyra, Louis Francisco / Wong, Tsz-Nga. 2019. Should the central bank issue e-money? Working paper 2019-003A, Federal Reserve Bank of St. Louis.

Keynes, John Maynard. 1930. A Treatise on Money, London: Macmillan.

Kindleberger, Charles P. / Laffargue, J.-P. (eds.). 1982. Financial Crises. Theory, History, and Policy, Cambridge University Press.

Krüger, Malte / Seitz, Franz. 2014. The Importance of Cash and Cashless Payments, Proceedings of the International Cash Conference 2014: The usage, costs and benefits of cash, www. bundesbank.de .

Kumhof, Michael / Noone, Clare. 2018. Central bank digital currencies – design principles and balance sheet implications, Bank of England Staff Working Paper, No. 725, May 2018.

Levine, Matt. 2019. The Fed versus the Narrow Bank, Boomberg Opinion, 8 March 2019.

Licandro, Gerardo. 2018. Uruguayan e-Peso in the context of financial inclusion, ppt, Basel University, 16 Nov 2018.

Macfarlane, Laurie / Ryan-Collins, Josh / Bjerg, Ole / Nielsen, Rasmus / McCann, Duncan. 2017. Making Money from Making Money. Seigniorage in the Modern Economy, publ. by New Economics Foundation, London, and Copenhagen Business School.

Mai, Heike. 2015. Money market funds, an economic perspective, db research, EU Monitor Global Financial Markets, 26.2.2015.

Mathew, Neil. 2018. Bitcoin Cash Surpasses Paypal’s Transaction Speed, Newconomy, November 12, 2018.

Mayer, Thomas. 2019. A digital Euro to compete with Libra, Flossbach von Storch Research Institute, Macroeconomics 02/07/19.

McLeay, Michael / Radia, Amar / Thomas, Ryland 2014: Money creation in the modern economy, Bank of England Quarterly Bulletin, 2014 Q1, 14–27.

McMillan, Jonathan. 2014. The End of Banking. Money, Credit, and the Digital Revolution, Zurich: Zero/One Economics.

Meaning, Jack / Dyson, Ben / Barker, James / Clayton, Emily. 2018. Broadening narrow money: monetary policy with a central bank digital currency, Bank of England Staff Working Paper, No. 724, May 2018.

Minsky, Hyman P. 1982. The Financial Instability Hypothesis. Capitalist Processes and the Behavior of the Economy, in: Kindleberger, C.P./ Laffargue, J.-P. (Eds.): Financial Crises. Theory, History, and Policy, Cambridge University Press, 13–39.

Minsky, Hyman P. 1986: Stabilizing an Unstable Economy, New Haven: Yale University Press.

Murrau, Steffen. 2017. Shadow money and the public money supply: the impact of the 2007–2009 financial crisis on the monetary system, Review of International Political Economy, Vol. 24 (5), September 2017, 802–838.

North, Michael. 1994. Das Geld und seine Geschichte vom Mittelalter bis zur Gegenwart, München: C.H.Beck.

O’Brien, Denis Patrick. 1994. Foundations of Monetary Economics, Vol. IV – The Currency School, Vol. V – The Banking School, London: William Pickering.

O'Brien, Denis Patrick. 2007. The Development of Monetary Economics, Cheltenham: Edward Elgar.

OMFIF/IBM. 2019. Retail CBDCs, the next payments frontier, London: Official Monetary and Financial Institutions Forum / Costa Mesa, CA: IBM Blockchain Worldwire.

Positive Money. 2011. Bank of England Creation of Currency Bill, London: Positive Money.

Ryan-Collins, Josh / Greenham, Tony / Werner, Richard / Jackson, Andrew. 2012. Where Does Money Come From? A guide to the UK monetary and banking system, 2nd edition, London: New Economics Foundation.

Schemmann, Michael. 2012. Liquid Money – the Final Thing. Federal Reserve and Central Bank Accounts for Everyone, IICPA Publications.

Shiller, Robert J. 2015. Irrational Exuberance, revised and expanded 3rd edition, Princeton NJ: Princeton University Press.

Siekmann, Helmut. 2016. Deposit Banking and the Use of Monetary Instruments, in D.Fox/ W.Ernst (eds). Money in the Western Legal Tradition. Middle Ages to Bretton Woods, Oxford University Press, 489–531.

Simmel, Georg. 2004 [1900]. Philosophy of Money, ed. by David Frisby, London/New York: Routledge.

Skidelsky, Robert. 2018. Money and Government: The Past and Future of Economics, New Haven/London: Yale University Press.

Summers, Lawrence H. / Stansbury, Anna. 2019. Whither Central Banking? Project Syndicate, Aug 23, 2019.

Sveriges Riksbank. 2017. The Riksbank's E-Krona Project, Report 1, Stockholm, Sep 2017.

Sveriges Riksbank. 2018. The Riksbank's E-Krona Project, Report 2, Stockholm, Oct 2018.

Sveriges Riksbank. 2018b. Special issue on the e-krona, Sveriges Riksbank Economic Review, 2018:3.

Tapscott, Don / Tapscott, Alex. 2016. Die Blockchain Revolution, New York: Penguin Random House LLC.

Turner, Adair. 2019. Central banks have lost much of their clout. Monetary policy is no longer enough to keep the economy on track, Financial Times, 23 August 2019.

Wortmann, Edgar. 2019. Public depository: safe-haven and level playing field for book money, Working paper, Stichting Ons Geld, Netherlands.

Zarlenga, Stephen. 2002. The Lost Science of Money, Chicago/Valatie, NY: American Monetary Institute.

Download the entire paper (parts I and II)

as a PDF >

Contents

Dominant currency and dominant money

Taxonomy and hierarchy of money

Tidal changes in the composition of the money supply. Like ebb and flow

From around 1900 until today: rising tide of bankmoney, ebb tide for central-bank money

Download the entire paper (parts I and II)

as a PDF >