Government Debt and Monetary Financing

The current end of a debt supercycle. Looming debt crisis

Most countries in today's world system are nearing the end of a decades-long large wave of sovereign debt (Fig. 1).

Fig. 1 Secular wave of government indebtedness Japan, USA, UK, Germany 1940/50 – 2010/15

The wave represents the rising branch of a debt supercycle. The cycle is not only about government debt, but also one of private debt, including financial institutions, companies and households. For example, the US government debt was 120% GDP in 2022, but the nation's total public and private debt was 300–350% GDP (Figures 2 and 3).

Fig. 2 National-debt supercycle USA 1925–2022

Fig. 3 Debt supercycle USA by debtor categories

Let us focus on the recurring over-indebtedness of government. In earlier times, this was due to the costs of the military and warfare, infrastructure, and the pomp and splendour of the courts of kings and princes. Today, this is still true to a certain extent with regard to the military and infrastructure. Otherwise, however, the costs of welfare and health have come to the fore, as well as education, science, technological and economic development. Overall, a considerable part of the various departmental expenditures directly or indirectly benefits the economy, education and employment. Similarly, a large part of government spending is of a compensatory nature, that is, the government has to spend money on services, infrastructures and transfer benefits that are considered necessary, but for which there is a lack of private investment and other private expenditure.

Part of government spending is almost always debt-funded. Given the existing high levels of taxes and welfare contributions at 35-45% GDP, these can hardly be expanded any further (tax resistance). Recurrent plans of debt containment or even debt reduction mostly ended in still more debt. Most recently, in the 2010s, this was mainly due to the banking crisis and euro debt crisis since 2008. With the 2020s, a mix of new crisis developments occurred, especially the end of cooperative globalisation (the free-trade expansion of cross-border chains of production and provision) and its overturning into new great-power confrontation, furthermore the manifest climate crisis, in addition a shortage of labour supply as a result of demographic change and shorter working hours, the three-years Covid crisis, and Russia's assault on Ukraine in February 2022. All this has triggered further surges in government spending and thus expanded public debt (Fig. 4).

Fig. 4 Failed attempt to curb government debt in the 2010s

The Economist 8-10-22, Special Report, p.4

The new crisis developments are associated with shortages in the factor supply and output. This has triggered an unprecedented jump in inflation, from previously ±1% CPI by 2021 to around 10% in 2022, and above in middle- and low-income countries. At the same time, central banks want to end the financial repression of the 2010s, which was keeping interest rates artificially low, even below the then low inflation rate, through Quantitative Easing. That resulted in a glut of reserves and bankmoney. The now rising interest rate level meets a weakening economy. This leads to stagflation, i.e. economic stagnation together with rising inflation, and rising interest rates. This makes the mountains of debt a menacing colossus that threatens to collapse when governments are no longer able to service public debt and interest rates on the bond market skyrocket.

The normal course of a debt crisis

There is no yardstick for over-indebtedness. What is certain, however, is that in an environment of stagnation combined with higher interest rates, highly indebted states will sooner or later find themselves in the awkward situation of having to default. It is about time to get honest about government debt: "Debts that can't be paid, won't be paid" (M. Hudson). This is a matter of fact, with the implicit call to do something about the matter. The spectrum in this respect ranges between policies of harsh austerity on the one hand and demands for debt relief on the other. Both are feasible to a degree, but counterproductive on a larger scale.

Debts can only be cancelled to the extent that the creditors have equity capital that is reduced by the cancellation of the debt. If a creditor were to waive too many claims, its equity would become negative and the creditor thus insolvent. In most state bankruptcies, therefore, a multi-pronged approach is taken:

1) Only a smaller part of the debt is cancelled.

2) The rest is rescheduled, partly deferred, and extended over a longer period of time.

3) A more or less harsh austerity regime is imposed on the debtor, possibly with the appropriation or pledging of real assets.

In other cases, comparatively high debt is by no means interpreted as over-indebtedness. Nation-states with great economic power are granted much higher debt levels than others. Such states can continue to roll over their debts, even expanding them by replacing maturing old bonds with new ones.

One example is Japan, with the world's highest public debt at 227% GDP in 2022, compared to 177% in Greece, which was imposed a tough austerity regime. Another example is the US, which also has a high debt-to-GDP ratio of 124%. The USA has never reduced its national debt in total since 1835, only temporarily relative to GDP in phases of strong economic growth coupled with high inflation. At the same time, the absolute national debt of the USA continued to rise year after year. In spite of this, the US dollar became the world's reserve currency in the 20th century and US Treasury bonds are considered a 'safe haven'.

Harsh austerity regimes are counterproductive

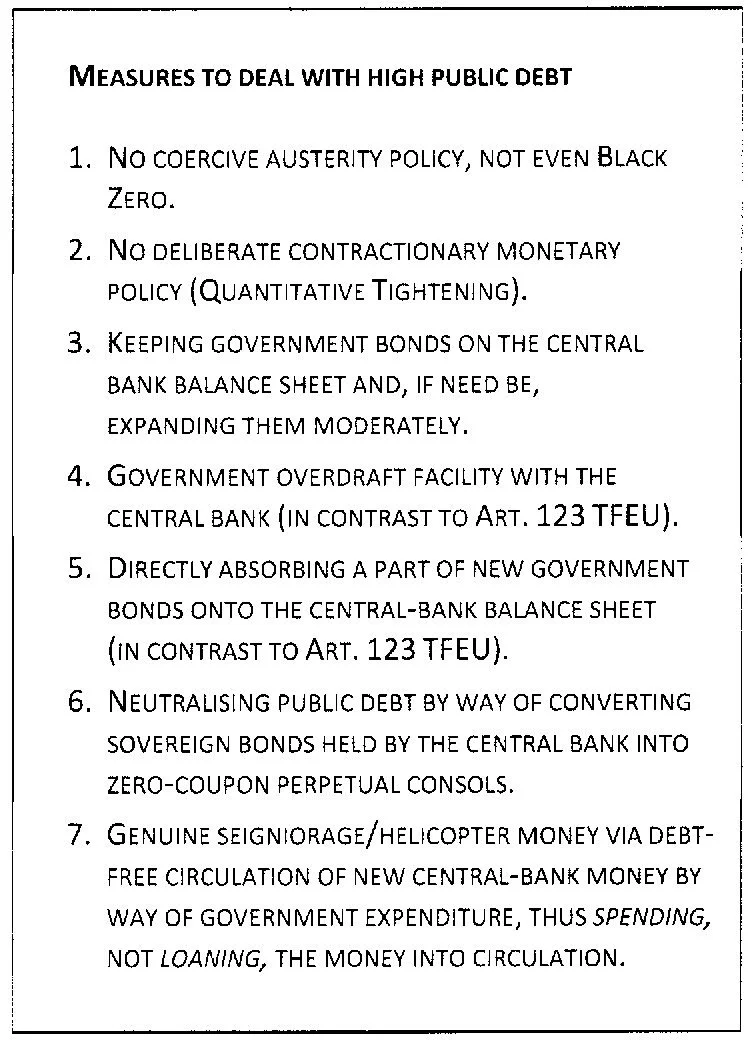

Imposing harsh austerity (to make the debt serviceable) may seem understandable from the creditors' point of view. Normally, however, insisting on austerity budgets is counterproductive. Shrinking government spending usually leads to shrinking economic growth and the over-indebted state will therefore be even less able to meet its liabilities in the long run and to become a good debtor again. Even the seemingly moderate Black Zero policy in Germany from 2013 to 2019 proved to be self-damaging, both in terms of investment in infrastructure and economic development as well as in terms of public services, especially education, health and also defence. Against this background, the first of seven measures in a sovereign debt crisis is to refrain from imposing harsh austerity policies.

1. No coercive austerity

In terms of government policy, avoiding austerity means not to reduce budgets and not to increase taxes, but to maintain government spending as far as possible and, if necessary, even expand it, incurring more debt. Harmful policies such as Black Zero or even budget surpluses in the midst of difficult times must not be repeated.

2. No contractionary monetary policy (Quantitative Tightening)

For the central banks, renunciation of austerity means that the monetary policy of Quantitative Easing since 2008 (expansion of the monetary base through open-market purchases of government bonds) should not be followed by Quantitative Tightening (reduction of the monetary base). Every net repayment of monetary credit means extinguishing money. On a significant scale, this would have just as bad consequences today as in 1929–33.

3. Keeping sovereign bonds on the central-bank balance sheet and, if need be, expanding them moderately

Instead of reducing their holdings of sovereign bonds, central banks should retain these holdings and, if necessary, continue to expand them moderately. Contrary to widely held opinion, this is not in itself monetary financing of government expenditure. It is banks, shadow banks, pension funds, insurance companies and households that are being refinanced here. They are the private holders of sovereign bonds. For sure, their refinancing facilitates the continued issuance of government bonds and stabilises the bonds' market value and level of interest.

The prohibition imposed on state central banks to directly contribute to government spending. Honi soit qui mal y pense

Today, the government of an EU member state has no choice but to borrow from banks and other private investors. Any other form of financing public debt is prohibited. For funding current government expenditure, levying taxes is the only other designated way. According to prevalent legal opinion, the prerogatives of a sovereign state include monetary sovereignty. In fact, however, while there is a national unit of account, the privilege of money creation today rests largely with the banking sector, supported by the central bank, while the treasury and parliament are not allowed to issue money (except by means of an antiquated prerogative of coinage). Likewise, the ECB and national central banks are prohibited from granting credit to the government or from purchasing sovereign bonds directly from the government. Only indirect retroactive open-market purchases from private holders of bonds are allowed.

In the EU, this is laid down in Art. 123 TFEU (Lisbon Treaty). A similar rule exists in the United States. Other market economies have not formally imposed such a prohibition. With Art. 123 TFEU, the state disadvantages itself and privileges those banks that act as primary dealers of government bonds, to some extent also subsequent financial intermediaries. Government bonds are a good deal for financial investors, less so for the taxpayer. Such being the case, the demand arises to make monetary financing - that is, direct central-bank contributions to funding government expenditure - possible again to a certain extent. To that end, repealing or amending Art. 123 TFEU is indispensable.

4. Government overdraft with the central bank

An amendment to Art. 123 TFEU allows for the reintroduction of an adequate overdraft facility at the ECB for the governments of euro member states. Prior to the Maastricht and Lisbon treaties even the monetarily restrictive Bundesbank granted bridging credit to the federal governments of the time to smooth out temporary gaps in the tax flow. During their EU membership, the British had insisted on maintaining the government's overdraft facility with the Bank of England (ways and means advances). In times of crisis, especially from 2008 onwards, this has proved to be a useful and flexible instrument of direct monetary financing.

5. Directly absorbing a part of new government bonds onto the central-bank balance sheet

Furthermore, the ECB and other central banks in the EU should be authorised to absorb a certain portion of newly emitted sovereign bonds directly onto their balance sheets, for example 15–20% of the respective bond issue. This is proven practice in Canada. It works smoothly.

Neutralising public debt

The problem of high government debt at high interest rates cannot be eliminated by any financial trick. However, the problem can be defused. This can be done by

6. converting sovereign bonds held by the central bank into zero-coupon perpetual consols

Instead of rolling over government debt at maturity, sovereign bonds held by the central bank ought to be consolidated, and thus neutralised, on the central-bank balance sheet by converting them into zero-coupon perpetual consols, that is, bonds free of interest and without fixed maturity. In the present untenable situation, such neutralisation of sovereign debt on the central-bank balance sheet is technically simple and pragmatically obvious. Whether the central bank bought the bonds in question directly or on the open market is irrelevant.

The bonds in question are to become formally interest-free, because in actual fact that's what they are: The interest paid by the treasuries to the central bank flows back to the treasuries with the central-bank profit. As for the principal, however, the bonds remain a liability of the government to the central bank. The national debt continues to exist. But the central bank holds its claims on the government in abeyance for an indefinite period. The respective part of the national debt is put on hold, deactivated, neutralised in this sense. The central bank, as creditor, retains the right to reactivate the debt, in other words, to call in the bond credits in question. Privately held government bonds remain unaffected and continue to bear interest and be repaid.

Genuine seigniorage / helicopter money

The most straightforward way of monetary financing – and the one that most clearly corresponds to monetary sovereignty – is to transfer newly to be issued central-bank money (= legal tender = sovereign money) directly to the treasury.

7. Debt-free issuance of new central-bank money by way of government spending

This means that part of the new money to be issued would come into circulation debt-free through public spending, as genuine seigniorage, whether in the form of conventional reserves (central-bank book money in use by state bodies and banks only) or as retail central-bank digital currency (CBDC) in the form of digital tokens. The central bank must determine the quantities involved on grounds of monetary policy not directly subjected to fiscal criteria and independent of government directives. Monetary policy may cooperate with budgetary and fiscal policy, but not under fiscal dominance, and only to the extent that nothing stands in the way in monetary terms. The other part of new central-bank money would continue to come into circulation through central-bank credit to financial institutions and through open-market operations. These channels remain necessary to a certain extent in order to be able to readjust the money supply flexibly and also at short notice.

The practice of putting official money into circulation directly through public spending or per-capita allocation (nowadays called helicopter money), instead of exclusively through central-bank credit to banks as is the case today, was by no means uncommon until the early decades of the 20th century. In America, for example, the British governors of the later United States issued colonial bills in the 18th century, similar to princely and royal treasury notes in Europe. This was followed by the continental dollars of the American War of Independence and the greenbacks as well as greybacks of the American Civil War in the 19th century. Thereafter, the U.S. government issued Treasury notes (although decreasing compared to Federal Reserve notes) until the 1970s.

Contrary to a widespread stereotype, this did not normally involve over-issuance and inflation. Where this did occur, if at all, it had to do with counterfeiting and wartime circumstances. Today's dominant private bankmoney creation, by comparison, is recurrently overshooting, entailing asset inflation and consumer price inflation.

Monetary accountancy

Unlike former treasuries, today's central banks have a little accounting problem with providing new money by way of genuine seigniorage. This was apparent, for example, in the question of how to provide helicopter money to the people, a measure that was also considered by some central banks around 2015/16. The accounting catch is this. A central bank cannot 'just like that' transfer new central-bank money to the government or households and firms. Under the accounting and reporting standards followed internationally today – GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards) – a central bank is treated like any commercial bank, not as a monetary authority wielding a state's monetary sovereignty.

Central banks, like banks, cannot enter the money they create into their own books as a liquid asset. Instead, banks and central banks initially make funds available to their customers as account balances in 'disbursement' of a credit amount. On the banks' balance sheet, this is represented as a liability to the borrower and as a claim on the borrower (asset) to pay interest and repay the principal. Banknotes and book money ('deposit' money) begin to exist by being credited and thus lent into circulation. A pertinent usage speaks of credit money or debt money or credit-and-debt money. This has led to the false identity of money and credit and to the exposure of the monetary system to the risks of finance – a source of perpetual instability, a fundamental flaw of the existing monetary system, which is essentially a bankmoney regime. This structural fault must be remedied anyway, especially with regard to independent central banks under state law in the exercise of a nation's or community of nations' monetary sovereignty. One possible approach is to add a central-bank currency register upstream to the central bank's operational balance sheet (see How to account for sovereign central-bank money).

The paper as a PDF >

Contents

The current end of a debt supercycle.Looming debt crisis

The normal course of a debt crisis

Harsh austerity regimes are counterproductive

Genuine seigniorage / Helicopter money

The paper as a PDF >