Does finance no longer need money?

On the links between money and credit, in response to a study sponsored by the Swiss Bankers Association

Introduction and summary

The Swiss Bankers Association has sponsored a study on sovereign money.[1] Its apparent intention is to rebuff the Swiss popular initiative on Vollgeld (i.e. sovereign money, or central bank money, respectively). The initiative has effected a popular vote to be held on the question of whether to restitute the prerogative of money creation from the banking sector to the Swiss National Bank.[2]

The study parades scientific scholarliness, which, however, turns out to be a hollow claim. This not only applies to the flawed reception of the initiative's reform program, but equally to the Banking School doctrine held in the study. For the sheer number of objections and corrections to be made, a detailed criticism of the study would come out as a rather long-winded exercise.[3] So this paper focuses on discussing a central topic, which is decisive for the validity of both the Bacchetta study and the sovereign money approach. That topic is the link between money and credit, and their role in the development of crises in banking and finance.

The Bacchetta study asserts the neutrality of bank credit and bankmoney – thus, in a way, their financial and economic insignificance – on the grounds of an alleged general decoupling of credit from money according to another study by Schularick/Taylor. An 'age of credit' is said to have replaced the previous 'age of money'. Correspondingly, control of the stock of money by the central banks, as advocated by the Vollgeld-Initiative, is deemed pointless for stabilising banking, finance, and the economy.

In the following, the core hypothesis of the Bacchetta study is disproved in five aspects.

1. The general hypothesis of a decoupling of credit from money is muddled and definitely wrong with regard to bank credit and bankmoney. Within the existing system of bank credit money, the stocks of outstanding bank credit and the stocks of bankmoney are inextricably tied to one another.

2. The empirics of the study are based on erroneous assumptions and a questionable database.

3. What is actually shown empirically is ongoing monetary overshoot, i.e. the GDP-disproportionate expansion of money, financial assets, and debt, especially bank credit and bankmoney, with destabilising consequences.

4. The overall stocks of credit, financial assets, and corresponding levels of indebtedness exceed the banking sector's volumes of primary bank credit, in that secondary credit – that is, financial intermediation among nonbanks on the basis of bankmoney – creates additional financial assets and liabilities of nonbanks. These, however, remain essentially anchored to the stock of bankmoney, because secondary nonbank credit does not normally create money of its own and cannot act as a substitute for bankmoney, or only marginally so.

5. The 'decoupling' that has actually taken place is the loosening tie of bank credit (bankmoney) to central bank credit (central bank money), and thus a much-reduced dependence of banks on central banks. As a result of the system-determining role of pro-active primary bankmoney creation, conventional instruments of monetary policy are no longer sufficiently effective. Stabilising banking and finance thus requires – as demanded by the Swiss sovereign money initiative – the central banks to retake full control of money creation (not, however, taking control of banking and the uses of money).

Bank credit and bankmoney. The astounding thesis of their disconnectedness

Regarding the interplay between money and credit, the Bacchetta study holds a position that defined the British Banking School almost 200 years ago. In the 1830–40s, the School defended the bankers' private privilege of note issuance, standing against the Currency School of the time, whose representatives wanted to achieve monetary and financial stability through an arrangement that would ensure central bank control of money issuance.

Ever since, the banking industry asserts the neutrality of credit money issued by the banks (then private banknotes, today bankmoney-on-account). Any causation of crises by overshooting bankmoney creation (= excessive extension of bank credit) is denied. Bank credit and bankmoney are not seen as a cause of inflation or overheating in business cycles, resulting in crises of over-investment and over-indebtedness; today also, and more importantly, taking the form of asset inflation in financial cycles and ensuing financial crises.

In the same vein, the Bacchetta study again rejects any link between money creation, economic cycles, and crises, which is in fact the usual attempt to assert the financial and economic neutrality of bankmoney, if bankmoney creation is not contested altogether. In the Bacchetta study, even the link between money and credit is denied ('there is no correlation between changes in money and changes in credit in Switzerland').[4]

The purpose of such positing is to invalidate a basic tenet of sovereign money reform and the underlying monetary system analysis, which is that central-bank control of the stock of money enables the stabilising credit and finance. 'The defenders of sovereign money clearly worry about credit, but they want to control it by controlling money'.[5] The study declares pointless any attempt to exert overall control of credit and debt by overall control of the stock of money. Remarkably, this also comes down to saying that any conventional approach to monetary policy is futile. The study does not explicitly pretend the market would adjust things by itself, but the woolly way of arguing insinuates that crises cannot really be prevented or mitigated, while at the same time ruling out any problem with fractional reserve banking.

As proof of the alleged disconnectedness of money and credit, Bacchetta relies on another study by Schularick/Taylor in which the authors put forth the hypothesis of 'a decoupling of money and credit aggregates … As credit growth has increasingly decoupled from money growth, credit and money aggregates are no longer two sides of the same coin'. The meaning thus is that credit is decoupling from money. An earlier 'age of money' in the development of financial capitalism is said to have been supplanted by a present 'age of credit'.[6] This is supposed to be shown in Figure 1.[7]

Before coming to the empirics of Figure 1, a basic flaw in the underlying theory or model must be pointed out. 'Bank loans' exceeding 'broad money' is interpreted as proof of credit decoupling from money since about 1990. In the Bacchetta study, moreover, this is embedded in the currently fashionable opinion according to which anything of monetary value (i.e. anything that has a price, especially any securitised item) can itself be used as money. Talking in this way, however, contributes to confusion rather than clarification. Most importantly, that fashionable opinion does not belong in the context of bankmoney and bank credit (Figure 1), but relates to secondary credit among nonbanks as discussed below.

In view of the pure credit money system as it stands today, any hypothesis of a decoupling of bank credit from bankmoney is a mistaken assumption. Bankmoney is bank credit-borne money, that is, bankmoney is credited by a bank into a customer bank account, which we then use today as the preferred means of payment. Bank credit cannot escape bankmoney, because the money comes with the credit. In an analogous way, this also applies to central-bank credit to banks, which creates 'reserves' on a central-bank account, that is, the means of cashless payment in the interbank circuit.

Moreover, customer deposits (bankmoney) cannot serve as loanable funds for banks. Bank credit cannot be extended by lending deposits of customers A to customers B. Commercial banks do not act as financial intermediaries, i.e. middlemen between savers and borrowers, as a long-standing fallacy about modern money and banking still has it.[8] What banks can do is creating, de- and reactivating, and finally deleting bankmoney, but banks cannot use themselves their customers' bankmoney. For re-financing their own lending and investment business, banks need central-bank reserves and cash. Only nonbanks use bankmoney in financial and real-economic transactions with other nonbanks, as explained when discussing secondary credit below.

Money creation by credit extension is often referred to as the 'identity of money and credit'. Taken literally, the formula is misleading because money and credit are two different things. It applies nonetheless that the extension of credit and the creation of a corresponding amount of money are carried out in one act, and in the end both the redemption of the credit and the deletion of the money. It is all the more important to see that money and credit are two different things fulfilling different functions. The credit is not the money; if it were, the respective holder of the means of payment would at the same time be the debtor of the crediting bank, which they are not (while it is true at any time that the holder of a bank deposit is a cash creditor of the bank). Bankmoney, as any money, is circulating among subsequent bearers, while the money borrower (the bank debtor) remains the same all the time. That which functions as money is not the credit contract, but the currency units entered into a debtor's bank account. The terms for that money are interchangeable: bankmoney = bank credit-and-debt money = deposit money = bank deposits = all monetary liabilities of banks to nonbanks = all monetary claims of nonbanks against banks.

The amount of bank credit and the amount of bankmoney issued by way of disbursing the credit are equal to each other. Therefore, any postulate of disconnection between bank credit and bankmoney is doomed to fail. Both amounts might differ from one another only in that interest payments from customers to a bank result in the deletion of the amount of bankmoney involved, while the originating loans, as long as not repaid, remain claims outstanding. Seen from this angle, one would expect a somewhat higher level of bank credit than there is bankmoney – a problematique of its own, relating to interest payments in bankmoney as well as deactivated bankmoney, a compensatory constraint for extending new bank credit, and maybe even a general growth constraint. However, this is an unsettled issue, and as far as such a mechanism exists, it is at work at all times in the same way and thus cannot explain why prior to the 1970–90s 'broad money' appears to be higher than 'bank loans', and why since that point in time the tide would have turned so dramatically, given that the difference attributable to interest payments to banks could be expected to be relatively steady.

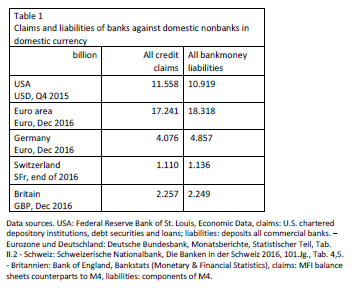

Beyond the question of customer interest payments to banks, it can indeed be assumed that the amounts of bank credit and bankmoney are basically the same. In Table 1, the monetary claims and liabilities of banks against nonbanks in a number of currency areas come out as largely corresponding to each other. Remaining incongruities should be reducible to statistics and international payment traffic. Most importantly, a general excess of bank credit over bankmoney does not exist. How could it be different in the present bankmoney regime?

Empirical pitfalls

The Schularick/Taylor hypothesis presupposes central categories of economics not to be as clearly defined, or as clearly used, as one would expect. Depending on language, paradigm preferences, and vested interests, 'credit' can refer to quite different things, even to student credit points for meeting course requirements. The prevailing narrative today is a supposed indeterminacy of terms such as money, credit and bank – once again astounding for a social science that strives for 'exactness'.

In Figure 1, 'broad money' means the monetary aggregate M2 or M3 or M4, depending on the country and time. 'Bank loans' means domestic bank credit to nonbanks. This excludes interbank credit on the basis of reserves, credit abroad and from abroad, as well as credit from nonbanks to other nonbanks (secondary credit by financial intermediation). Sources of error in the Schularick/Taylor database are likely to stem from both the delimitation between banks and nonbanks as well as the delimitations of the monetary aggregates.

The distinction between monetary financial institutions (MFIs = banks) and non-monetary financial institutions (non-MFIs) is basically clear-cut. Commercial banks create bankmoney. They do it whenever they make loans to nonbank customers or buy securities from them, or other items which the banks can account for as an asset. Disbursement of a loan or payment for a purchase is done by entering an according number of 'credits', i.e. currency units, into the customer's bank giro account – which then is the creation of an according amount of bankmoney. That bankmoney is not taken from somewhere else, but created in the act of crediting an account. The banks manage the bankmoney in sectoral cooperation by transferring the 'credits' in cashless payments among subsequent nonbank customers.

By contrast, non-MFIs do not normally create a means of payment, and certainly no bankmoney. Instead, they lend or invest already existing bankmoney. Depending on the country, however, it may be that certain financial firms are registered as a 'bank', being active in the loan and investment business, and subject to credit services oversight, but not admitted to central bank refinancing and the interbank payment system. This may apply, for example, to building societies, savings and loan associations, mutual banking cooperatives, or postal bank services.

Apart from that, many non-MFIs are run under the roof of a banking corporation, without being a commercial bank themselves, for example, money market funds, investment trusts, other types of funds, special vehicles for securitisation purposes, thus quite a few things which form part of investment banking. Such non-MFI operation units are not an immediate part of the corporation's commercial banking. They could also be run as independent non-MFIs. In the euro area, where universal banks are predominant, 48% of all assets in the financial sector are held by banks, i.e. by monetary and non-monetary operation units under the roof of a universal banking corporation; in Germany, France, and Italy the share is even higher at 66–72% of all financial assets.[9] It can thus be assumed that the excess of 'credit' over 'money' in Figure 1 is attributable to non-MFI financial intermediation rather than primary commercial bank credit.

Regarding the bankmoney in Figure 1, the non-uniform meaning of 'broad money' is likely to be another source of error. Depending on the currency area and years in consideration, monetary aggregates come with different and changing definitions. What is more, most monetary aggregates do not include further monetary bank liabilities, in particular long-term capital formation of nonbanks with banks, and also the wholesale volumes of money market fund shares (MMF-shares). For example, U.S. dollar M2 or euro M3 include retail MMF-shares only and exclude wholesale MMF-shares.

Seen from this angle, even 'broad money' is too narrow in the context of the decoupling hypothesis. Long-term monetary capital represents bank liabilities as much as deposits in M2/M3. Considering the spectrum of monetary claims and liabilities – from liquid ones to less liquid and non-liquid positions at long-term maturity – cutting off some part of the spectrum is an arbitrary reduction. All banking liabilities to nonbanks represent bankmoney. Had Schularick/Taylor also included the long-term and wholesale bank liabilities to nonbanks, and made sure there were no non-MFIs being treated as banks, the 'bank loans' in Figure 1 would hardly have exceeded 'broad money'.

GDP-disproportionate bankmoney creation

If Figure 1 does not show the alleged decoupling of bank credit from bankmoney, what then is to be seen there? An unprejudiced look at the chart in fact unveils a highly relevant finding, that is, the strong expansion of bank credit and bankmoney co-directional or pro-cyclical and disproportionate to GDP, except for the contractive 1930–40s era of depression and war. For the period from 1870 to 1929, and from the 1950s through to the 2000s, however, the GDP-overshooting supply of bank credit and bankmoney is patently obvious.

Table 2 contains additional figures on the growth in real and nominal GDP and GDP-disproportionate increases in bankmoney (monetary aggregates).

As the figures show, the active stock of bankmoney M1 as well as the (mostly) inactive stocks M2–M4 increased in strong disproportion to GDP, disproportionate also to nominal GDP which includes inflation. Bankmoney expansion in the U.S. seems to have been overshooting the least. This is deceptive, because since around 1980 MMF-shares were introduced in the U.S. very expansively. MMF-shares are an additional money surrogate, based on bankmoney rather than central-bank money. MMF-shares can be transferred much like bank overnight deposits, and became widely used as an alternative to bankmoney, especially in financial-market transactions, in order to circumvent interest ceilings on bank deposits imposed at the time by the Federal Reserve.[10] At the beginning of the crisis in 2007/08, MMF-shares amounted to 2.5 times the amount of M1 (in Europe MMF-shares represented 'only' a third of M1).[11]

Another way of evincing GDP-disproportionate bankmoney creation is shown in Table 3. According to a common textbook consideration, money circulates in a certain temporal rhythm, especially a monthly rhythm, thus about 12 times a year; some parts of the money circulate more often, other parts less often. Seen like this, an active stock of money of about 1/12 of nominal GPD (incl. inflation) would be sufficient for carrying out all GDP-contributing transactions in the real and financial economy. In actual fact, however, the active money supply M1 in 2008 was much higher. The overshoot factor in the right column results as four to five times the expectable 1/12 of GDP. The seemingly lower factor in the U.S. can again be ascribed to the widespread use of MMF-shares.

In view of Tables 2 and 3, the question arises of why or for what the overshooting bankmoney supply was created, considering that much less money in circulation would have been enough to pay for the growth in GDP, including inflation and GDP-contributing finances. The answer is straightforward. The bankmoney overshoot fed and continues to feed into the expansion of non-GDP-contributing finance as well as in asset inflation and bubble building on financial markets such as commercial and residential real estate, stocks, commodities, derivatives, and 'alternative' investments.

Primary monetary credit by the banking sector and secondary non-monetary credit through financial intermediation among nonbanks. Financialisation

GDP-overshooting creation of bankmoney at first relates to transactions between banks and nonbanks. In its subsequent circulation in the public circuit, the bankmoney serves as the preferred means of payment among nonbanks (while the means of payment in interbank circulation is central-bank reserves). The public circulation of bankmoney not only enables real-economic transactions, but equally serves as the money base for financial transactions of and with non-MFIs.

This is no special aspect of 'macroeconomics', as the Bacchetta study repeatedly asserts in an attempt to distract focus from bank money. Instead, this is about the difference between primary monetary bank credit, which creates bankmoney (and prompts fractional refinancing in central bank money if need be), and secondary non-monetary credit among nonbanks on the basis of bankmoney. Secondary credit does not normally create additional means of payment (money surrogates), but it does create additional volumes of credit, of monetary claims and debt.

Non-MFIs playing a role in this are, for example, investment funds of all kinds, pension fundsm private equity funds, sovereign wealth funds, securitisation vehicles, insurance companies, more recently also fintech (crowdfunding, P2P-platforms, and others). Big financial intermediaries like Blackrock, DWS, Fidelity, or several sovereign wealth funds are now bigger and more influential than many banks, or they form part of the investment banking divisions of large banking corporations (for example, G.P. Morgan, Goldman Sachs, UBS, Barclays, DGS Singapore). Financial intermediaries such as funds, however, are run as separate non-MFI units. A fund is not a bank, just as a bank is not turned into a fund by owning one. Whether the investment branches of a bank are truly separate units or just a department of the commercial bank, ultimately depends on whether the payments of a respective unit are made in bankmoney managed through a bank giro account, or made in reserves through the central-bank account of the commercial bank.

The distinction between commercial bank and investment bank dates back to the second Glass-Steagall Act on separate banking in the U.S. from 1933 in reaction to Black Friday of October 1929. The law separated deposit taking, management of accounts and payments, and retail lending (i.e. commercial banking) from securities and other financial investment activities, wholesale banking, and wealth management (investment banking). This was thought to shield the customers' deposits from risky investment activities. Each bank had to opt for either 'commercial' or 'investment'.

After the Second World War, the American separate banking system was by and by watered down. At first, the investment banks J.P. Morgan and Goldman Sachs, lateron all investment banks, were permitted to act as commercial banks again, that is, as depository institutions, managing accounts and payments, and approved for refinancing at the Federal Reserve. Put differently, their 'license to print money' – bankmoney – was restored. The Glass-Steagall Act was completely repealed in 1999 by President Clinton. The separate banking system, however, was less important than might appear at first sight. Investment banks were always allowed to borrow from commercial banks for creating investment leverage. By softening and repealing Glass-Steagall, it simply became easier to create the desired degree of leverage.

In any case, since around 1980 – when globalisation took off, international flows of money and capital were deregulated, and investment banking became hypertrophic – nonbank financial intermediaries in tandem with commercial banks have engaged in a massive expansion of financial markets. This is the context where the fashionable opinion originated according to which any securitised promise to pay or repay money can itself be used as money. But there is less to this than the usual gossip has it, and as far as it has a point, it is not exactly new. Medieval tally sticks or formerly private banknotes are examples of 'securitised' or otherwise documented promises to pay that were used as means of payment. This also applies to commercial bills as far as these are still used. Above all, today it applies to bankmoney, which is a promise to pay out cash or transfer the credits-on-account inside the bank or to customers at other banks. Legally, bankmoney is still a surrogate for central-bank money, which is legal tender, in contrast to bankmoney which is not. By habitual practice, however, bankmoney has become the predominant, general and regular means of payment, and thus is used as if it were money proper, even though it is not.

Regarding today's financial markets, there are two forms of payment by transfer of a securitised financial claim. For one, in large financial transactions, such as for example in company mergers, payment in money is frequently complemented by payment in financial assets, most often equity stakes. For another, financial market deals are frequently settled by the transfer of MMF-shares, as already mentioned, rather than the transfer of bankmoney.

MMFs were established in the U.S. in the 1970–80s, at first by non-monetary financial institutions on the basis of bankmoney. Since the 1980s, MMFs are also run under the roof of investment banks and universal banks, in an attempt to make up for business lost to non-monetary financial institutions. Nevertheless, MMF-shares and the less convenient transfer of securities do not change the fact that in most real-economic and financial transactions, as ever before, payment is due in money. The partially pyramidal structure of money and credit, be it collateralised or securitised, possibly also including their subsequent packaging, is in a way remindful of the shell game – but that which counts, rather than the shells, is the money beneath in final settlement of the game.

Historically, the more modern financial instrument is money rather than credit; money in the sense of a generally, regularly and predominantly-used token means of payment. It may well be the case that ancient forms of economy started with credit (on the basis of payment in kind), as early as in archaic societies more than 3,500 years ago. Money, however – as a means of payment, not just as a unit of account – was only introduced in the 7th century BC in ancient Greece. Money made any business, particularly credit, both much easier and more efficient than before. To be able to settle any kind of debt by payment in money was and remains the most potent market catalyst. A promise to pay, or pay back, can temporarily be useful, but it is the final payment in money which makes or breaks it all – not least in modern banking and finance.

Therefrom, proclaiming an 'age of credit' overriding a previous 'age of money' is mischievous. Money and credit have co-existed in mutual enhancement since antiquity, and they are bound to continue this way. What has changed in recent decades, however, is the disproportionate growth of secondary financial intermediation by non-MFIs on the basis of bankmoney.

What Schularick/Taylor have re-discovered, and what has gained attention in the crisis years after 2008, is the well-known fact that financial crises result from credit and debt bubbles, or, as this was framed in business cycle theory, that crises result from over-investment/bad investment and over-indebtedness. Recent research contributions explaining and empirically documenting anew this causation were made by Shiller, Minsky, and others.[12]

The hypertrophic growth of investment banking and financial markets since around 1980 is most often referred to as financialisation. A 'decoupling' of credit from money is in no way a characteristic of this. Financialisation is not only fueled by secondary credit of non-MFIs, but in the first instance by primary bank credit. In all industrial countries, the lion's share of primary bank credit in recent decades (72–80 per cent) went into three uses: first and foremost into real estate transactions and mortgages; secondly into leveraging other non-GDP-contributing financial investments (including credit funding of friendly and hostile mergers and acquisitions); and thirdly into the perpetual expansion of sovereign debt (the purchase of sovereign bonds).[13] Funding production and service companies and private households together represents only the remaining fifth up to a quarter of bank credit. The biggest demand for money is clearly in real estate and securities where huge volumes of assets and debt have to be paid up. In the process, real estate and housing markets, similar to commodity markets, have increasingly taken on the traits of a non-GDP-contributing investment in lucrative financial value, rather than being a GDP-contributing investment in creating use value.[14]

More than ever before these developments are based on the GDP-disproportionate expansion of primary bank credit, thus the creation of bankmoney, and its manifold circulation in secondary non-monetary financial transactions. In Bacchetta there are repeatedly statements such as (a) 'in general money is not created by credit', or (b) 'bank credit is unlikely to be the source of money creation at the macroeconomic level'.[15] Against the background of the explanations given above these sorts of hypotheses prove to be partly confused and partly wrong. Statement (a) applies to secondary credit by non-MFIs, but is wrong with regard to primary bank credit. Statement (b) is wrong anyway in that primary bank credit to nonbanks always creates bankmoney. In today's monetary system, money is exclusively issued by way of credit. Bacchetta states this in another place himself when he is wondering about the possibility of non-credit-borne and debt-free issuance of sovereign money.

The hypertrophy of bank credit also becomes apparent from the levels of indebtedness. Debt of firms and private and public households, not including the financial sector, rose in most countries from about 100–200% of GDP before 1990 to 300–600% when the crisis hit in 2008.[16] When including the financial sector's debt, the figures, depending on the country and a different composition of total national debt, rise by another 150–250 percentage points. In the most indebted countries such as Japan or the Netherlands, overall national indebtedness reaches over 500% to almost 700% of GDP.[17]

The counterpart to this is the face value of monetary and financial assets. Their market value – in many cases including value appreciation and a degree of asset price inflation beyond substantiated value increases – can exceed the face value considerably. In the U.S., for example, the market value of financial assets from the 1950s through to around 1980, not including real estate and houses, was oscillating sidewards at 4–5 times nominal GDP. Thereafter until the onset of the crisis in 2007/08, financial assets rose steeply to 10–11 times GDP.[18] Apparently, this was too much of a good thing. Levels of credit and debt are definitely overextended when financial claims can no longer be serviced by current income (GDP) and viable additional debt, which then triggers contractive dynamics of defaults, value adjustments (write-offs), insolvencies etc. So far, financial economics has no substatiated idea on the financial carrying capacity of an economy.

Advanced decoupling of bank credit from central-bank money

The generally misleading hypothesis of a decoupling of credit from money in a way still makes sense, even if that special meaning is not intended in Schularick/Taylor and certainly not by Bacchetta. That meaning is about the decoupling of bank credit from central-bank money. Bank credit creates bankmoney. Its re-financing in central-bank money, or, as some say, its 'coverage' with central-bank money, and thus the dependence of banks on cash and central-bank reserves, has decreased greatly over time.

First, cashless payment has been crowding out cash. Put differently, bankmoney has been crowding out central-bank issued money in the form of notes and coins. Depending on the country, the share of bankmoney is now at 85–97% of the money supply, while cash is currently down to 15–3%, and only the smaller part of the cash is used for regular payments. For the larger part, cash is hoarded as a safety buffer, of late also as a defence against the threat of negative interest on deposit money, or the cash circulates in the underground economy. Regarding the dollar and the euro, more than half of the cash is used abroad as a parallel currency.[19]

Secondly, the reserves, in particular the liquid excess reserves used in interbank payments, are just a kind of subset of bankmoney, in fact representing only a small fraction of it. As a result of ongoing market concentration in banking (ever fewer banks that are ever larger with millions of customers), the need for banks to have reserves has also diminished. Thirdly, computerisation and telecommunication in banking in general, and payment systems in particular, has much accelerated interbank clearing and the velocity of reserve circulation in the interbank circuit.

By and by, each of the three processes has contributed to reducing the banks' dependence on central-bank money. As a result, the 100% of bankmoney in the euro banking sector today just needs about 2.5% central-bank money, of which 1.4% cash, about 0.1% liquid reserves, and 1% largely idle minimum reserves.[20] In some countries the re-financing need is even lower (e.g. Britain, which has no minimum reserves) or somewhat higher (e.g. the USA, which has higher minimum reserves). Smaller banks need relatively more excess reserves than bigger ones, as outgoing and incoming payments in larger banks are offsetting each other better than in smaller banks.

The present money system can be characterised as a state-backed private bankmoney regime; state-backed because accomodated at any time by the respective central bank to any fractional amount, and warranted, if in trouble, by both central bank and government. The pro-active primary bankmoney creation by the banking sector fully determines the resulting provision of central-bank money as well as the possible credit multiplier in secondary financial intermediation – whereas such a credit multiplier does not exist with regard to primary bank credit. A bank-related multiplier can be calculated as an arithmetic exercise, but this does not reflect an actual causation in a true process, and has not done so ever since the former cash economy disappeared about a hundred years ago.

As a consequence of pro-active bankmoney creation and the fractionality of the central-bank money base, the conventional instruments of monetary policy have largely lost effectiveness. Monetary quantity policy pursuing M1–M3–related growth targets is pointless if bankmoney creation is pro-active. Such quantity targets were questionable anyway, as they made the means (the money) an end in itself, which it is not – a fundamental mistake of the gold standard as well as monetarism.

In view of a refinancing rate of ±2.5 units of central-bank money on 100 units of bankmoney, the lever of monetary base rate policy is too short to be effective. What remains is a degree of corporate price administration, in that many banks tie some lending rates, particularly for overdrafts and mortgages, to recent interbank money market rates (lending and borrowing of excess reserves) over which a central bank retains a high degree of control. For the rest there is the modern augury of forward guidance. This means central banks notifying the markets of their expectations about the future development of interest rates and inflation. The impact solely depends on the public's firm belief in the central banks' divinations.

The 'decoupling of credit from money', in the form of bank credit and bankmoney creation becoming ever more detached from central-bank money, applies to a greater extent than many people involved in the process want to see or admit publicly. The predominance of bankmoney, after all, is the illegitimate and dysfunctional capture of the sovereign prerogative of money creation. The prerogatives of (a) determining the currency of the realm, (b) creating the money denominated in that currency, and (c) benefiting from the gain thereof (seigniorage), are of the same importance as the prerogatives, or say monopolies, of legislation, jurisdiction, territorial public administration, taxation and the use of force.

Instead, money creation today is determined by the banking sector, whereby the banks do not, and actually cannot, exert monetary 'control'. They just follow their individual business model and the trends and interests of the day. In consequence, self-limiting negative market feedback between demand and supply is overlaid by non-limiting positive feedback dynamics of money creation and increasing credit and debt on the one hand, and growing asset volumes and asset price inflation on the other. As a result, financial crises have become more frequent and severe than they have formerly been.[21] This is what the Vollgeld-Initiative wants to change by enabling control of the stock of money, because money comes with primary credit and serves as secondary credit thereafter. The central bank – as an independent monetary authority – must be able to pursue effective monetary policies, which requires control over money creation, and the continual readjustment of the money supply according to current developments in interest rates, prices, asset inflation, growth, and a number of additional relevant variables.

The false identity of money creation and credit extension. Their separation by sovereign money

Banks just taking care of their own business and not caring about the overall money supply is basically all right; or rather, it would be all right, were it not for the false identity of money creation and credit extension. As things stand today, banks bear primary responsibility for money creation, but they do not and cannot really act responsibly in this regard, and if in systemic trouble most banks are not really held responsible. They can still expect to be 'saved', be it by the central banks (acting as accommodating fractional refinancers of the banks and even as a bad bank for problematic bank assets), or by government bail-out, and now also by customer bail-in, i.e. compulsory recapitalisation by switching customer deposits (liabilities) into bank equity (bank capital).

Why does the banking sector enjoy such illegitimate feudal privileges? Because the banks control the bankmoney, which is the money of the people, firms and largely even public households and which stands or falls on the banks' balance sheets. In a way our money is held hostage to the banks' balance sheets; but it is not that the banks use our money, rather it is us who use bankmoney, unavoidably so under current circumstances. From there, the entire private and public economy is much more dependent on the banks than would be the case in a credit economy without the false identity of credit extension and bankmoney creation.

This is why the Vollgeld-Initiative aims at separating money creation from bank credit. The respective central bank as national monetary authority shall be entrusted with the exclusive prerogative of money creation, thereby establishing sovereign central-bank money in any technical form (cash, on account, or digital currency) as legal tender. This would easily keep apart what is dysfunctionally amalgamated today, that is, money creation and banking, separating money creation and overall control of the stock of money from the basically market-mediated uses of the money in banking, finance and real-economic transactions.

Separation of money creation and banking was already the program of the Currency School in the 1830–40s. The Currency School achieved an institutional arrangement for controlling the stocks of banknotes, which were then the increasingly predominant but still private means of payment. The vehicle for this was the gold standard, generally accepted at the time, but soon proving inadequate for modern money and industrial dynamics, and rightly of no more relevance today. Historically of much more importance and lasting relevance was something else, which is, putting an end to the unstable-volatile issuance of private banknotes and replacing them with the note monopoly of the national central banks.

Not taken into consideration at the time, however, was the interbank clearing of claims and liabilities on bank giro accounts (deposits), and the transfer of bank deposits as a way of cashless payment (even though the matter was touched upon in the Currency vs Banking controversy, and Adam Smith had addressed the subject half a century earlier). The mass proliferation of cashless payment by transfer of bankmoney only took place over the course of the 20th century. Today, the banks' credit money is by far the dominating means of payment, while the role of central-bank cash is declining ever more. It is therefore about time to take again the step that was taken in the 19th century relating to banknotes, today relating to bankmoney, that is, substituting sovereign money-on-account for public circulation, and perhaps also sovereign digital currency, for private bankmoney.

Sovereign money can be issued, and ought to be for the most part, like coins were formerly issued, that is, as genuine seigniorage by way of government spending, or by per capita dividend as some would prefer. When the money is spent, not loaned into circulation, it is, at source, not interest-bearing and without maturity. A smaller part of newly created money is likely to be issued by way of interest-bearing short-term credit to banks and perhaps to other financial institutions, too, serving open market operations for continually and flexibly readjusting the available stock of money. In any case, all of the sovereign money, including the part issued free of debt, will have a price attached to it – that is, interest – on the money and capital markets. In a monetarised and financialised economy, and particularly in a sovereign money system, interest rates are the most important of all prices which preferably ought to be market-borne and not be subject to price administration. It is more appropriate to provide an adequate stock of money – in a stable, though not fixed, but flexibly readjustable way – and leave the respective interest rates to the markets.

Meanwhile, it looks as if the solid cash of old is bound to be replaced not only by bankmoney, but also by digital cash in digital 'wallets', allowing direct payment from one such wallet into any other without a bank as 'trusted third party' comes into play.[22] It is all the more important to make sure that the new technical form of money will spread as central-bank issued digital currency, rather than initially as private money again (Bitcoin and the like) which would cause notorious problems until we remember that money is no private affair, but a public matter of constitutional importance.

Literature

Arslanalp, Serkan / Tsuda, Takahiro. 2012. Tracking Global Demand for Advanced Economy Sovereign Debt, IMF Working Paper, WP/12/284.

Baba, Naohiko/McCauley, Robert N./Ramaswamy, Srichander. 2009. US Dollar Money Market Funds and Non-US Banks, BIS Quarterly Review, March 2009 65–81.

Bacchetta, Philippe. 2017. The Sovereign Money Initiative in Switzerland: An Assessment. Arbeitspapier. Swiss Finance Institute / CEPR / Université de Lausanne.

Barrdear, John / Kumhof, Michael. 2016. The macroeconomics of central bank issued digital currencies, Bank of England, Staff Research Paper No. 605, July 2016.

BIS. 2015. Digital currencies, prep. by the BIS Committee on Payments and Market Infrastructures, Basel: Bank for International Settlements.

Dietz, Raimund. 2011. Geld und Schuld, eine ökonomische Theorie der Gesellschaft, Marburg: Metropolis.

Broadbent, Ben. 2016. Central banks and digital currencies, http://www.bankofengland. co. uk/publications/Pages/speeches/2016/886.aspx.

Bundesbank. 2015. Zahlungsverhalten in Deutschland 2014, Frankfurt: Bundesbank.

Bundesbank. 2017. The role of banks, nonbanks and the central bank in the money creation process, Bundesbank Monthly Report, Vol. 69, No. 4, April 2017, 13–30.

European Central Bank. 2016. Report on financial structures, Oct 2016.

Hilton, Adrian. 2004. Sterling money market funds, Bank of England, Quarterly Bulletin, Summer 2004, 176–182.

Huber, Joseph. 2017. Sovereign Money. Beyond Reserve Banking, London: Palgrave Macmillan.

Kindleberger, Charles P. 1993. A Financial History of Western Europe, New York: Oxford University Press.

Laeven, Luc / Valencia, Fabian. 2008. Systemic Banking Crises. A New Database, IMF Working Paper, WP 08/224.

Liikanen Report. 2012. High-level Expert Group on reforming the structure of the EU banking sector, chaired by Erkki Liikanen, final report, EU-Commission, Brussels, 2012.

McKinsey Global Institute. 2010. Debt and deleveraging. The global credit bubble and its economic consequences, January 2010.

McLeay, Michael / Radia, Amar / Thomas, Ryland. 2014. Money creation iin the modern economy, Bank of England Quarterly Bulletin, 2014 Q1, 14–26.

McMillan, Jonathan. 2014. The End of Banking. Money, Credit, and the Digital Revolution, Zurich: Zero/One Economics.

Minsky, Hyman P. 1982b. The Financial Instability Hypothesis. Capitalist Processes and the Behavior of the Economy, in: Kindleberger, C.P./ Laffargue, J.-P. (Eds.): Financial Crises. Theory, History, and Policy, Cambridge University Press, 13–39.

Minsky, Hyman P. 1986. Stabilizing an Unstable Economy, New Haven: Yale University Press.

Reinhart, Carmen M. / Rogoff, Kenneth S. 2009. This Time is Different. Eight Centuries of Financial Folly, Princeton University Press.

Rossi, Sergio. 2007. Money and Payments in Theory and Practice, London/New York: Routledge.

Ryan-Collins, Josh / Lloyd, Toby / Macfarlane, Laurie. 2017. Rethinking the Economics of Land and Housing, London: New Economics Foundation / Zed Books.

Schularick, Moritz / Taylor, Alan M. 2009. Credit booms gone bust. 1870–2008, National Bureau of Economic Research, Working Paper 15512. Reprinted in American Economic Review, Vol. 102, No. 2, April 2012, 1029–61.

Shiller, Robert J. 2015. Irrational Exuberance, revised and expanded 3rd edition, Princeton NJ: Princeton University Press.

Thiele, Carl Ludwig. 2017. Die Zukunft des Bargelds, Rede Forum Bundesbank, Frankfurt: Dt Bundesbank.

Turner, Adair. 2016. Between Debt and the Devil. Money, Credit and Fixing Global Finance, Princeton University Press.

Notes

[1] Bacchetta 2017, sponsored by the Swiss Bankers Association.

[2] For information on the popular initiative see http://www.vollgeld-initiative.ch/english.

[3] For a somewhat detailed criticism of the Bacchetta study by the Swiss sovereign money initiative see http://www.vollgeld-initiative.ch/medienmitteilungen/ einzel/harte-kritik-an-bezahlter-banken-studie-ueber-vollgeld.

[4] Bacchetta 2017 3.

[5] Bacchetta 2017 2, 3.

[6] Schularick/Taylor 2009 2, 5ff., 29.

[7] Schularick/Taylor 2009 6, Bacchetta 2017 3, 7f.

[8] Cf. McLeay/Radia/Thomas 2014, Bundesbank 2017, Rossi 2007 9–62, Huber 2017 57–100.

[9] ECB 2016, Table 2.1, 64.

[10] Baba/McCauley/Ramaswamy 2009, Hilton 2004, McMillan 2014.

[11] Huber 2017 111.

[12] Shiller 2015, Minsky 1982, 1986, Kindleberger 1993, Reinhart/Rogoff 2009.

[13] Liikanen Report 2012. Financial Crisis Inquiry Committee 2011. Turner 2016, 61. Arslanalp/Tsuda 2012 12. Huber 2017 111f. Positive Money, How much money have banks created? http://positivemoney.org/how-money-works/how-much-money-have-banks-created.

[14] Ryan-Collins/Lloyd/Macfarlane 2017.

[15] Bacchetta 20177, 4.

[16] McKinsey 2010 pp.10.

[17] McKinsey 2010 pp.28.

[18] Dietz 2011 201.

[19] Thiele 2017, Bundesbank 2015.

[20] The figures were derived from central bank statistics until 2008. Ever since, the aggregated data on reserves can no longer be directly referred to because the crisis policy of quantitative easing which has been flooding banks with reserves, distorting any 'natural' degree of reserve holdings.

[21] Laeven/Valencia 2008.

[22] On the topic of digital cash (digital currency) cf. BIS 2015, Broadbent 2016, Barrdear/Kumhof 2016.

The paper as a PDF >

Contents

Introduction and summary

Bank credit and bankmoney.The astounding thesis of their disconnectedness

GDP-disproportionate bankmoney creation

Decoupling of bank credit from central-bank money

The false identity of money creation and credit extension. Their separation by sovereign money

The paper as a PDF >